Idun Industrier: The Next Great Swedish Serial Acquirer That Nobody Talks About?

Sweden has produced the world's greatest concentration of Serial Acquirers. Idun is the most aligned of the emerging generation, under-earning today, and that gap is the opportunity. I have a position

Idun Industrier (IDUN-B ST) | Share price: SEK 330 | June 2026

Market Cap: ~3.8bn SEK/ ~€350mn | ADV: 2,350 shares/ ~€72k

Summary:

Idun Industrier is a Swedish serial acquirer with a simple model: buy niche, market-leading industrial businesses at 5-8x EBITA, keep them operationally independent, and redeploy the cash they generate into further acquisitions. Do that consistently, add 5% organic growth on top, and you compound at 15% annually. Idun has done exactly that since inception, growing attributable EBITA per share at 16.6% per year from 2016 to 2025.

The reason the stock is interesting right now is that Idun is under-earning on two fronts. Sweden’s manufacturing cycle has been in a trough since 2023, dragging organic EBITA growth negative in both 2023 and 2025. Alongside that, management has deliberately run the acquisition engine below capacity while prioritising balance sheet discipline. Both are temporary. The question is not whether this is a good business, as the track record shows that clearly. The question is whether the recovery plays out as the data suggests it should, and whether the current valuation adequately compensates for the uncertainty in the meantime.

I believe the growth slowdown is cyclical rather than structural, with gross margins having held stable at c.60% throughout the downturn, competitive positions intact, and the businesses most affected, those serving pulp and paper, heavy process industry and industrial maintenance, operate in markets where deferred work cannot be deferred indefinitely. The PMI data is turning, Q1 was strong, and management guided Q2 stronger still. When revenue starts returning, the operating leverage is material, as the 2020-22 expansion demonstrated.

At SEK 330 the business trades at c.16x run-rate EV/attributable EBITA, broadly in line with Indutrade and at a meaningful discount to the proven serial acquirers. The management alignment is among the best I have encountered in a listed company of this size. At the current multiple, if Idun delivers something close to its historical compounding rate, the stock should return c.15% per year from here. The upside case is more interesting: operating leverage as the cycle recovers, a couple of years of above-target organic growth, and a gradual re-rating as the track record lengthens and the stock gets discovered beyond its almost entirely Nordic shareholder base is a combination that could produce meaningfully better returns over a three to five year horizon. I am happy to hold at current price, and would look to add on any meaningful weakness towards SEK 300.

Background

Idun Industrier has been on my radar for some time. I first came across the name when I travelled to Stockholm in 2025 as part of ongoing research into serial acquirers, which are acquisition-driven compounders targeting at least 15% annual EBITA growth. I had more than ten meetings, back to back over two days, meeting large serial acquirers, emerging compounders and investors and brokers in the space. All shared a core, common focus on profitability, efficiency and growth, with varying approaches to get there. Success in this field requires the right mix of good people capable of making both operational and capital allocation decisions, wrapped in a high-performance culture and owner mindset. When I asked local experts which company they would put their own capital into, Idun was a name that kept surfacing as being of interest.

I have held a position ever since. With little written for public consumption on Idun, I finally sat down and did the work, and I thought I would add my thoughts to the public discourse for good measure. Here is what I found, and why I am happy to keep holding at the current price of SEK 330.

Sweden: The Spiritual Home of Serial Acquirers

For those unfamiliar with the asset class: Sweden has produced a remarkable concentration of acquisition-driven compounders, Lifco, Indutrade, Lagercrantz, Addtech, and a newer generation of challengers including Röko and Idun. This is not coincidence. Due to a confluence of factors, Sweden became the spiritual home of this movement: a rich industrial heritage dating back to the 19th century; a small and geographically isolated nation which was forced to embrace innovation and globalisation; a cohort of extremely wealthy families with a long-term ownership culture; a high-trust, high-transparency culture that makes acquisition transactions cheaper and less onerous than in most markets; and a culture of decentralisation that allows constant, stable development of acquired businesses. The result is giants like Lifco, Indutrade, Lagercrantz and Addtech that have compounded at high rates (often >20% CAGRs) for many years, large challengers like Röko, and now emerging compounders like Idun.

Note: REQ Capital are a leading voice in this space and have written well on this topic both in their book ‘The Compounders’ and in their other detailed writings on the space.

History, Founders & The Origin Story

Idun Industrier was founded by Adam Samuelsson in 2013. Adam had worked at Nordic Capital, one of Scandinavia’s most prominent private equity firms, buying and restructuring industrial companies before founding Idun. He has 20 years of experience investing in family-owned businesses and has been a board member at various companies including the Swedish compounder Bufab. The genesis for Idun came from Adam’s realisation while at Nordic Capital that instead of being forced to sell high-quality businesses every five to seven years in sync with the typical private equity cycle, just as they were really understanding the business’s key drivers and its potential, wouldn’t it be better to retain ownership and realise the potential of these businesses over the long term? In his own words, the idea was to keep and develop the fantastic businesses, rather than throwing the chips back on the roulette table.

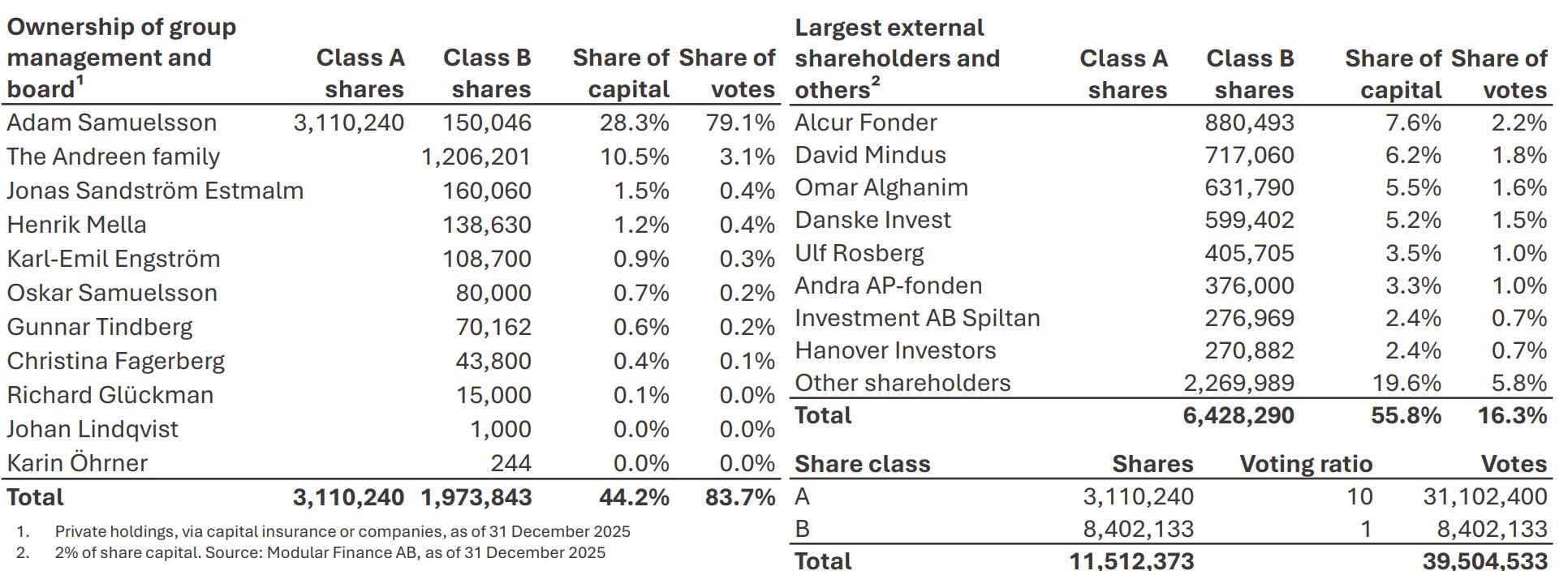

Idun was seeded with Adam’s own capital and that of several wealthy families from his Nordic Capital network, including Robert Andreen, one of Nordic Capital’s co-founders. The Andreen family are the second largest shareholder with 10.5% of share capital, with Robert’s son Ludwig sitting on the board. It is noteworthy that c.44% of the share of capital is owned by the group management and board.

Included in that cohort is Gunnar Tindberg, the legendary Indutrade CEO from 1978 to 2004, who owns 0.6% and also contributes his skills in dealmaking, developing people and experience to Idun as a long-term member of the board. Mr. Tindberg built Indutrade into one of Sweden’s outstanding serial acquirers completing c.50 acquisitions with an exceptional 95% success rate, driving a c.20% CAGR during his 26 years at the helm.

“During its first decade, cost consciousness was so strong that the (Indutrade) head office was based out of a basement in a residential building in the mid-sized town of Malmö in southern Sweden. The office didn’t even have a sign on the door.” -- Indutrade Chapter, The Compounders Book, REQ Capital

Henrik Mella serves as CEO, having taken over in 2024 from Karl-Emil Engström, who moved to Deputy CEO and Chief Business Development Officer. Henrik’s background spans McKinsey, Assa Abloy, CEO of Cale Group and Group Pricing Director at Husqvarna, and pricing expertise is a recurring theme among the best serial acquirers: small family businesses often have never thought systematically about pricing, and the gains can be material. As these operators might say, if you haven’t lost a customer, you haven’t raised prices enough.

The whole parent company team comprises eight people in two rooms in a non-descript building in Stockholm, who conduct all investment work themselves, from target identification all the way to negotiation and closing. Idun avoids external advisers unless absolutely necessary, ensuring the team knows the companies inside out while saving costs, with a head office cost of SEK 25mn, overseeing SEK 2.4bn of revenue across 20 businesses.

Business Model & Acquisition Strategy

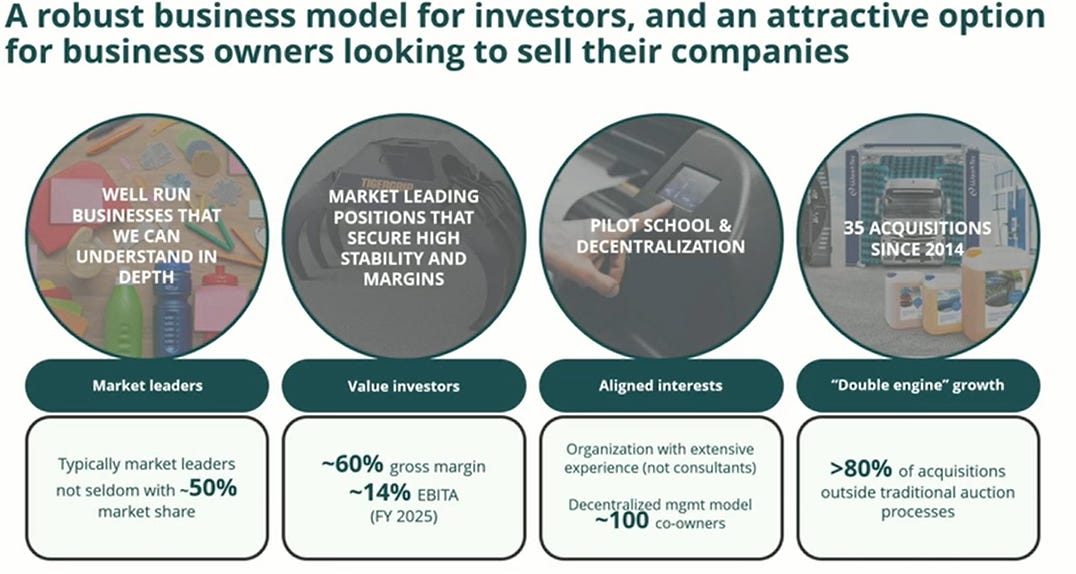

Idun is a decentralised acquisition-driven compounder. The model is straightforward in principle: acquire the majority stake of a target business, typically 70-90%, keep it operationally independent, extract the cash it generates, and redeploy that cash into further acquisitions. The difficulty is in the execution, which is why most attempts at this model fail and a few become compounding machines. Since inception Idun has acquired more than 35 companies across 20 group companies today.

The target company profile is specific. B2B industrial businesses in manufacturing, industrial trading or industrial services, with gross margins of c.60%, EBITA margins of c.14%, high market share often above 50% in their specific niche, and a track record of stability of profitability through multiple recessions. Many of Idun’s portfolio companies have been in business for over 100 years. Henrik has personally attended the centenary celebrations of two of them. Idun explicitly avoids consumer-facing businesses, turnaround situations and anything the team cannot understand thoroughly, preferring to tinker rather than make drastic changes and impose a new blueprint at companies they acquire.

Cultural fit matters as much as financial metrics. Idun looks for honest, reliable sellers who care about what happens to their business after the transaction, and has walked away from potential deals in the past because the fit was not right. Over 80% of deals are self-sourced, with the CEO and CFO regularly making cold calls to targets and building relationships over years rather than months. When the moment comes, those owners often choose Idun over a higher-bidding PE buyer because they know their business will not be flipped or reorganised. At a pace of only two to four deals per year on average, the team can afford to be patient and selective in a way that volume-driven acquirers cannot. They see themselves as value investors and typically pay 5-8x EBITA multiples, often including property. They have only ever sold one business, an aircraft maintenance company called TH Air, because a buyer emerged who was clearly a far better long-term home for it.

Idun compounds through three tools. New platform acquisitions at 5-8x EBITA are the primary engine, implying a day-one pre-tax return on invested capital of 12-20% before any organic growth. Bolt-on add-ons, smaller businesses absorbed into existing platforms, are a second tool. The third is ownership top-ups: buying out minority shareholders at pre-agreed valuation formulas embedded in the original shareholders’ agreement. In 2025 Idun increased its stake in Eugen Wiberger from 71% to 86% and in 2B Best Business from 70% to 98% through exactly this mechanism, essentially pre-purchasing future earnings at a known multiple in businesses they already know well.

Idun also owns SEK 264mn of property at book value across 28 properties and 98,000sqm, acquired alongside the businesses and held for the long term. Some carry environmental permits from the 1970s that create genuine barriers to entry, the market value is likely materially above book, and the portfolio provides a source of secured financing when needed.

The Businesses

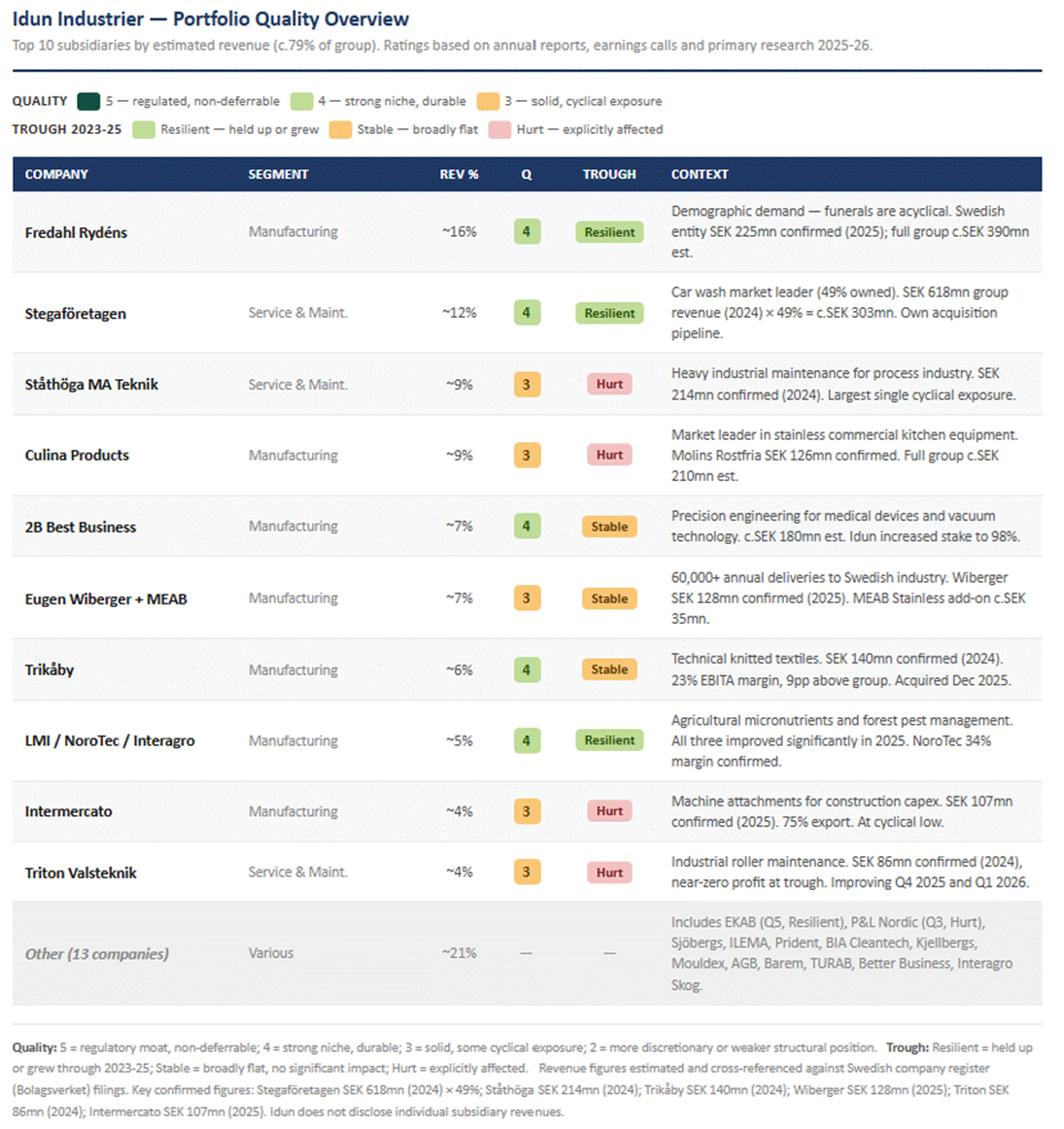

Deep in the Swedish countryside, in the small town of Asarp, sits the Fredahl Rydéns factory. They make coffins and urns. If you die in Sweden there is a 65% chance you will be buried in one of theirs. In Norway the figure is 84%. Demand is directly tied to deaths, roughly 91,000 per year in Sweden alone, which should only increase as the population ages. This is the kind of business Idun owns, a dominant business in a specific, overlooked niche, with a dominant competitive position.

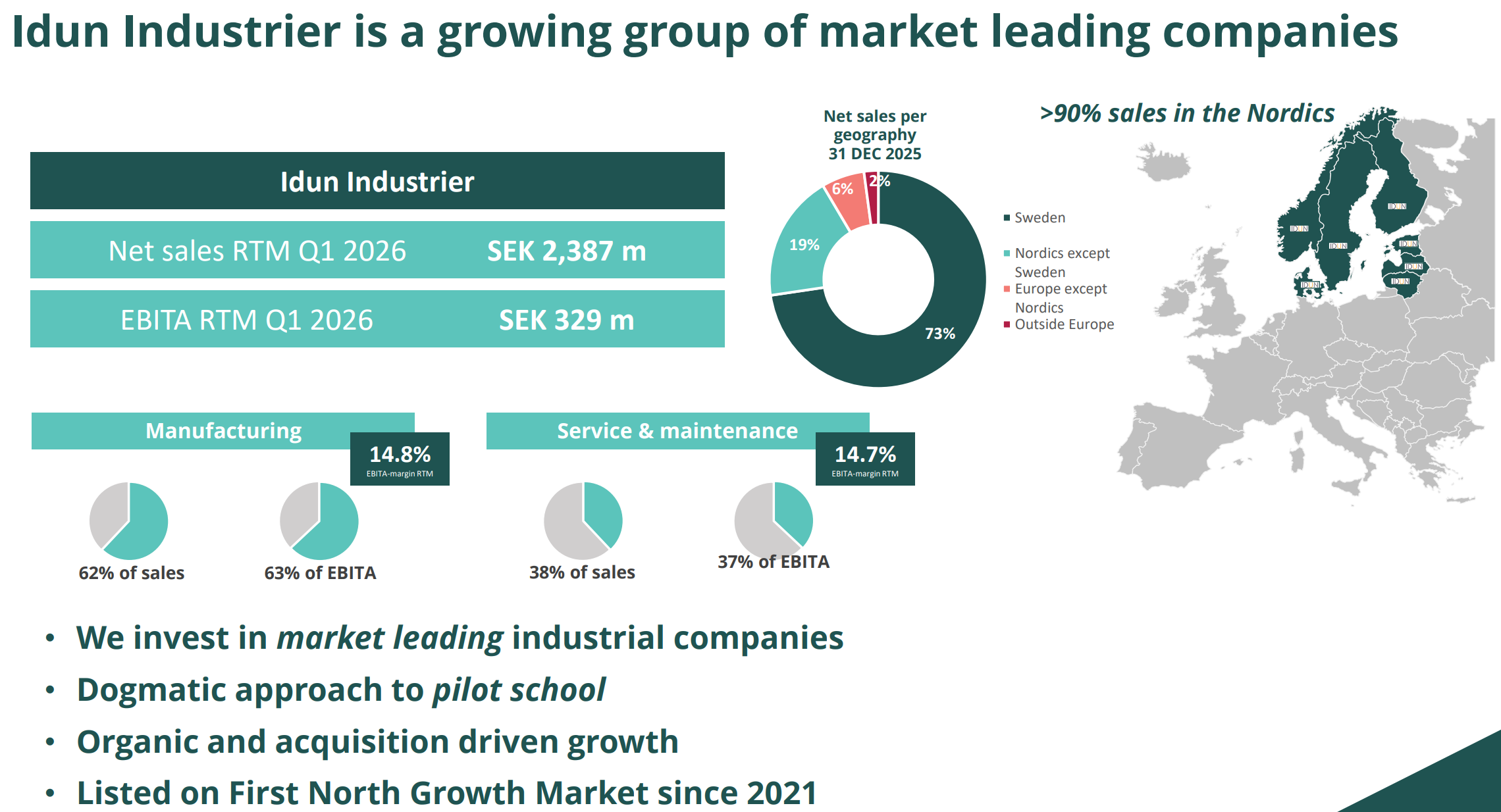

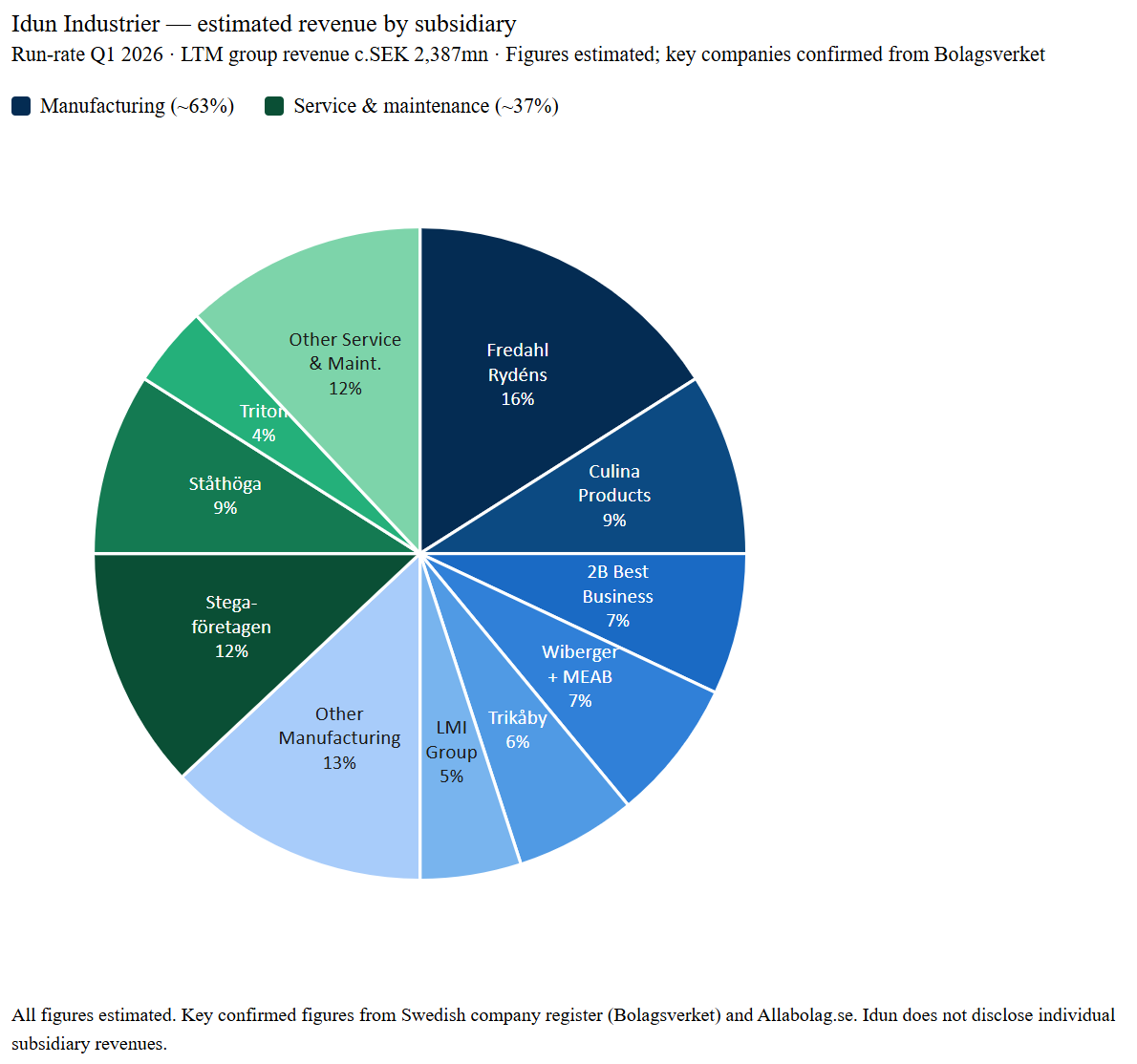

Idun currently operates 20 group companies across two segments, c.60% manufacturing and 40% service and maintenance, with more than 90% of revenue from the Nordics. The portfolio is eclectic: a precision engineering manufacturer making high-specification components for medical devices and vacuum technology, an industrial fastener distributor making 60,000 deliveries a year to Swedish factories, a provider of high-voltage maintenance for critical Stockholm buildings, a Nordic market leader in coffins. What they share is high market share in their respective niches, strong margins and long track records of profitability.

An example of a higher quality business is EKAB, employing c.20 certified electricians maintaining high-voltage infrastructure for hospitals, data centres and buildings in Stockholm that legally cannot lose power. The service is mandated by regulation with a 24/7 response requirement, and once you have route density across Stockholm it becomes effectively uneconomic for a competitor to replicate. With growing revenue and approaching a 30% EBITDA margin, EKAB is essentially unaffected by fluctuations in the business cycle, and represents the prototypical type of business that Idun would like to own.

At the other end of the quality spectrum sits Better Business, a mystery shopping and compliance monitoring service. Idun has acknowledged that this business proved vulnerable when customers cut discretionary spend during the downturn, the service not being non-negotiable in the way that regulated maintenance or funeral products are. It has been an underperformer, and is not the type of acquisition Idun will seek to replicate.

The portfolio spans that full quality spectrum, but is on balance considerably better than that contrast might suggest. At the top sit businesses with regulatory, demographic or contractual demand that is either non-deferrable or genuinely acyclical: EKAB, Fredahl Rydéns, Stegaföretagen’s car wash operations and the LMI group’s agricultural micronutrients and forest pest management products. Below that sits the majority of the portfolio, solid niche industrial businesses with defensible positions and often some cyclical exposure.

Recent acquisitions signal where the portfolio is heading. Trikåby, acquired in December 2025, runs at a 23% EBITA margin, nine percentage points above the group average. AGB, the most recent deal, runs at a c.22% EBITDA margin, servicing and calibrating pipe-pressing tools for plumbers who are required by insurance companies to have them regularly checked, which is as close to a captive recurring revenue stream as you find in a small industrial business. The table below gives the full picture for the group’s companies.

Incentives & The “Pilot School”

“We have invested, absolutely most of them have, in our own shares. For me personally as well. In terms of looking at listed companies like us in Stockholm, this clear cut alignment of interest that we have created from external shareholders to the board of directors, the management group, to the management group in each and every one of those 20 companies, it is quite hard to replicate.”

- Henrik Mella, CEO, Redeye Serial Acquirers Conference 2026

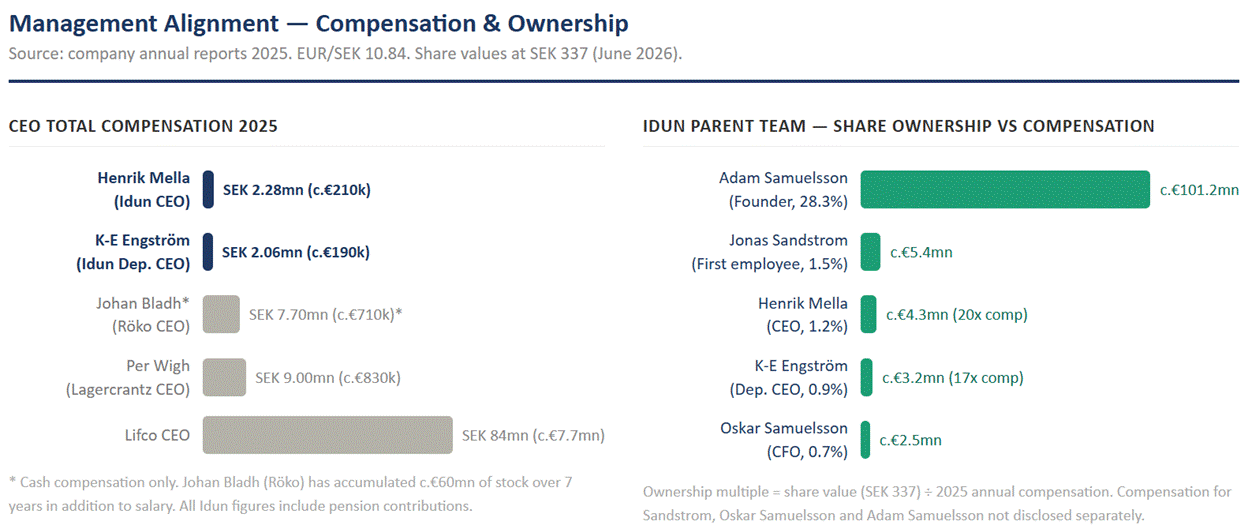

Idun is among the most comprehensively aligned public companies I have encountered. Mella’s total compensation in 2025 was SEK 2.28mn, c.€210k including pension, a figure that speaks for itself for a CEO, when set against the peer comparison below. There is no variable remuneration for anyone at the parent company level beyond a modest warrant programme, and their wealth, like that of any outside shareholder, accrues through the share price over time. I think of Idun less as a conventional listed company and more as a family office executing an acquisition-driven strategy.

The management team all hold shares: Mella 1.2%, Jonas Sandström (first employee) 1.5%, Karl-Emil Engström 0.9%, CFO Oskar Samuelsson 0.7%. There has been some insider selling from Mella, Engström and Adam Samuelsson over the past year, each small relative to their total stakes. Warrant programmes are modest and market-priced, with maximum dilution across all outstanding series of less than 0.8% of shares.

The board reinforces the same ethos, with every board member a shareholder. The anchor investors from the 2021 IPO prospectus, the Andreen family (10.5%), David Mindus of Sagax (6.2%), Omar Alghanim, a Kuwaiti businessman (5.5%), and former Nordic Capital partner Ulf Rosberg (3.5%), are all still there which signals their conviction. The investor base is almost entirely Nordic, with Hanover Investors at 2.4% the only notable non-Nordic institutional name.

The alignment extends into all twenty group companies through what Idun calls the Pilot School. In every group company without exception, local management has personal ownership, ranging from production managers to MDs, with over 100 co-owners having taken stakes of typically 1-3%, often funded through personal loans.

When Idun acquires a business, the founder typically retains a minority stake under put/call arrangements that activate after three to five years. In practice they tend to stay far longer: the original owner of Intermercato was approaching retirement when Idun bought 70% of the business and is still there over a decade later. As Idun gradually buys out minorities, the share of group EBITA attributable to ordinary shareholders drifts upward, and currently stands at c.83%.

Overall, the alignment of interests between external shareholders and the people running this business is as tight as I have encountered in any listed company of this size.

Financials: Performance & Capital Structure

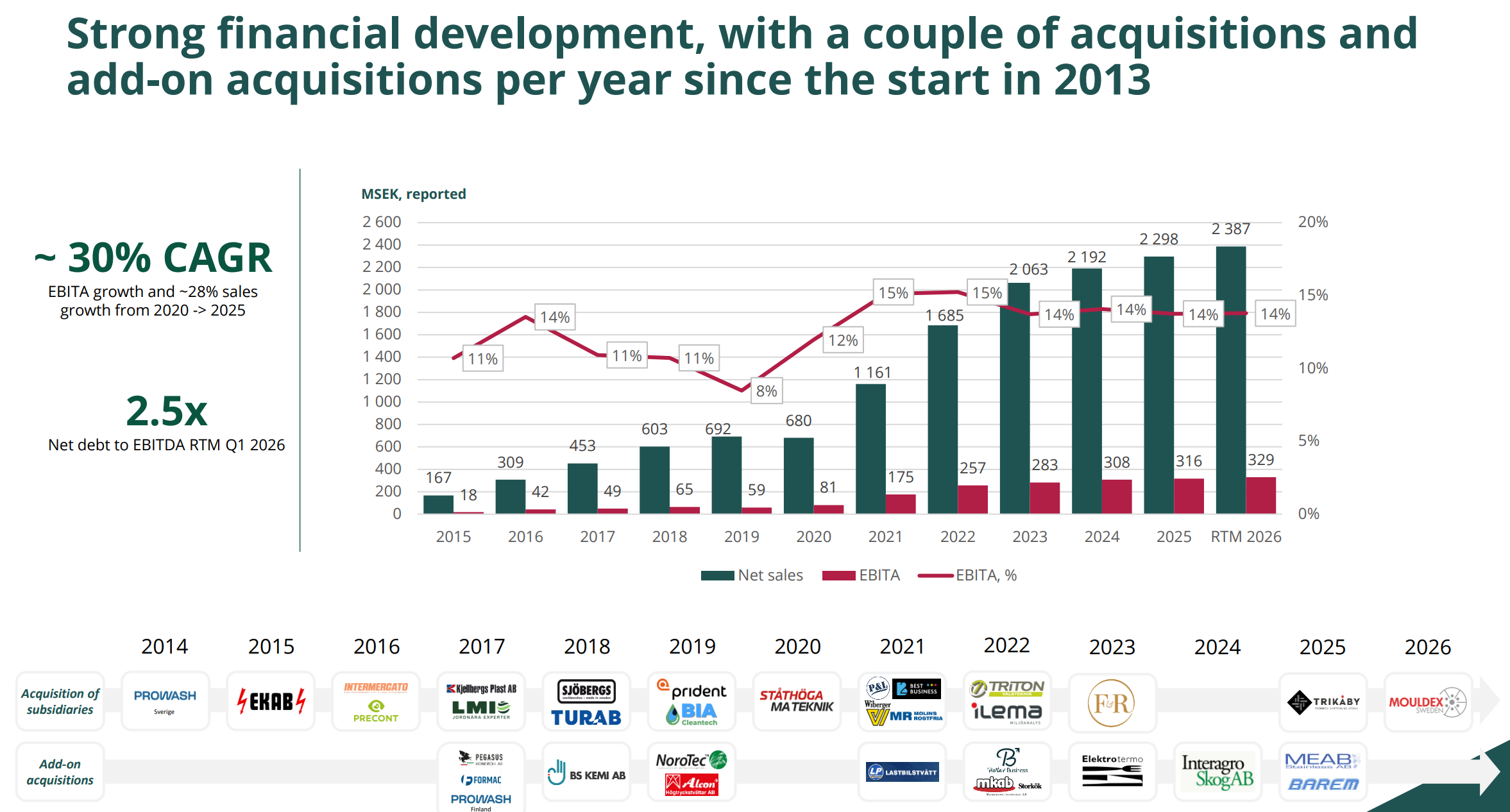

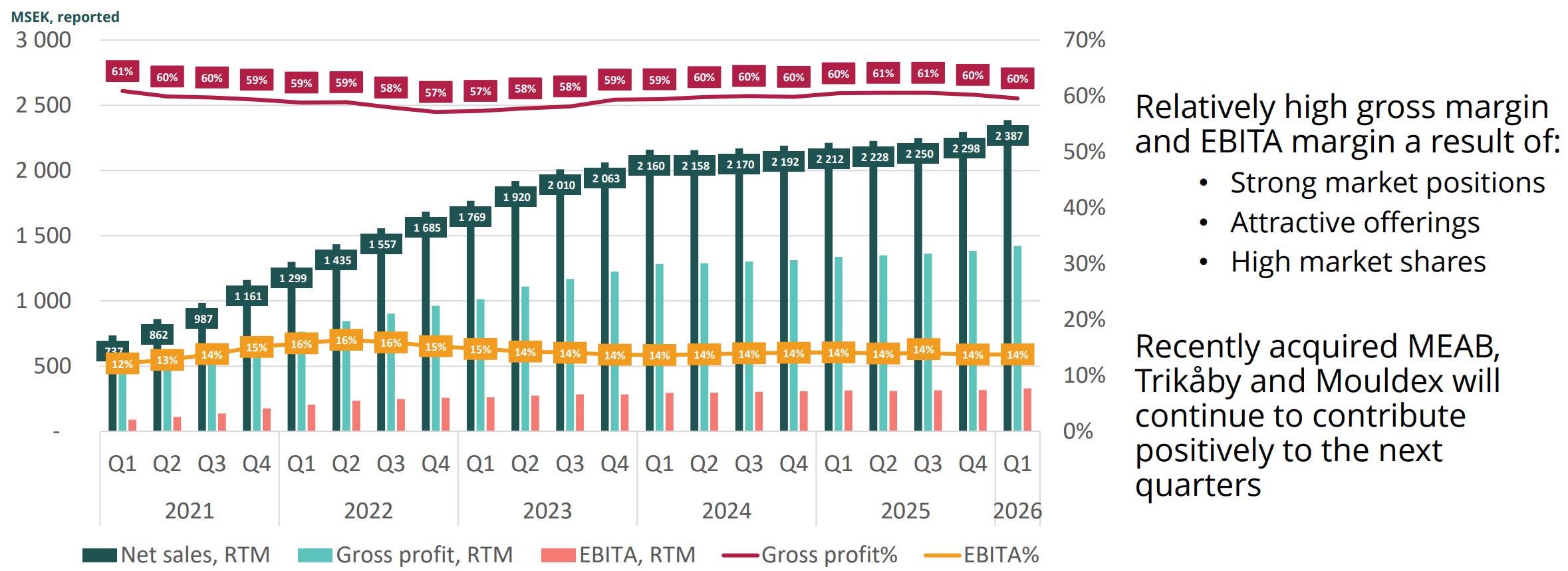

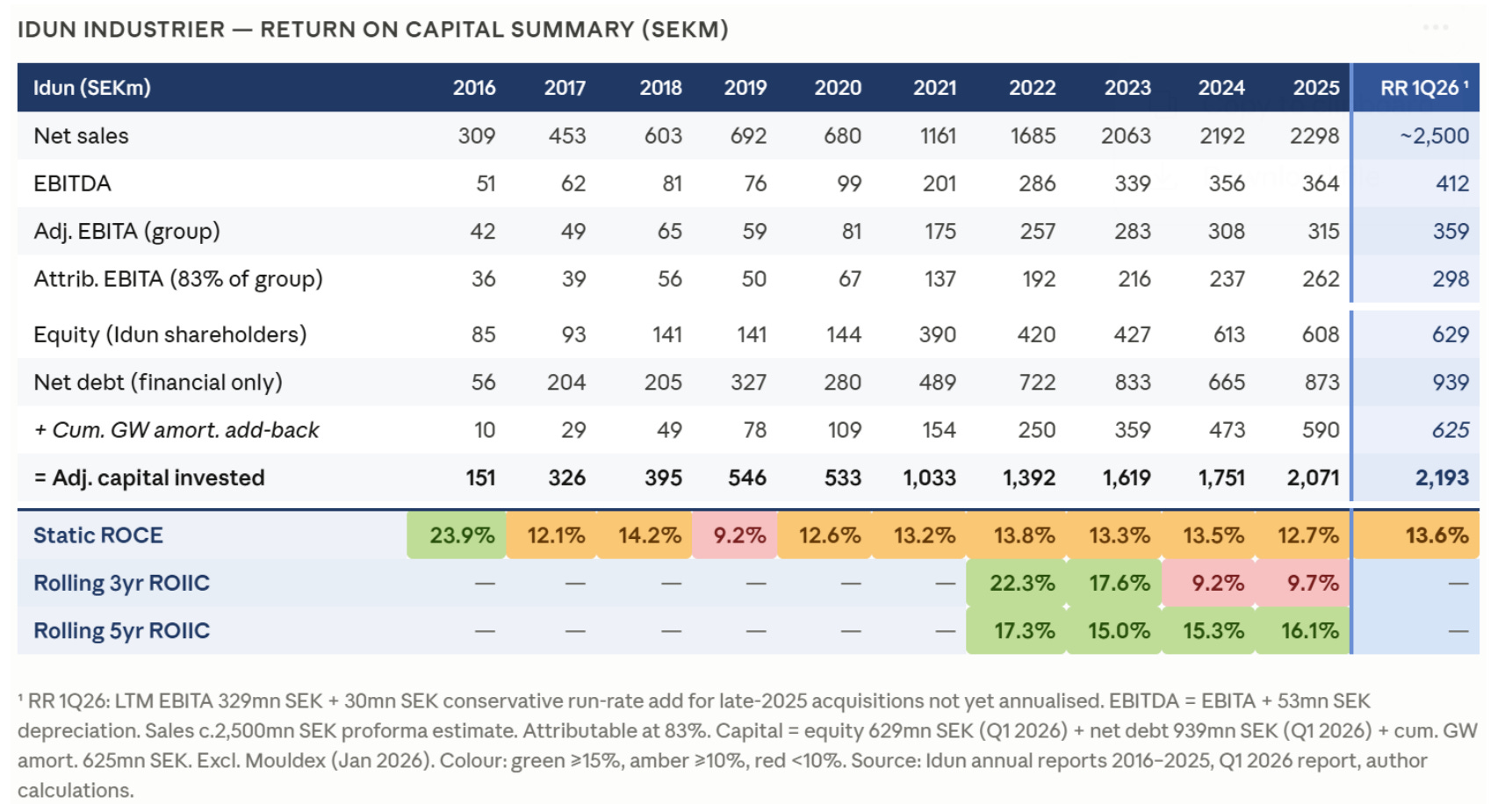

As of Q1 2026, Idun has LTM revenue of SEK 2,387mn and LTM EBITA of SEK 329mn, implying a 14% EBITA margin. Gross margins have been remarkably stable at c.60% across the full history, and EBITA margins have expanded from 10.7% at inception in 2015 to c.14% today, through a COVID year, a post-pandemic boom and a Nordic industrial downturn. That stability through the cycle is the clearest available signal that the portfolio quality is genuine. It should also be noted that Idun likely benefits somewhat from owning the property at many of its companies, which suppresses the rental cost line.

Q1 2026 net sales grew 15.7% to SEK 659mn with EBITA of SEK 91mn, up 16.8% year on year, the strongest Q1 on record. Organic sales growth was 5%, and management guided Q2 to be stronger than Q1.

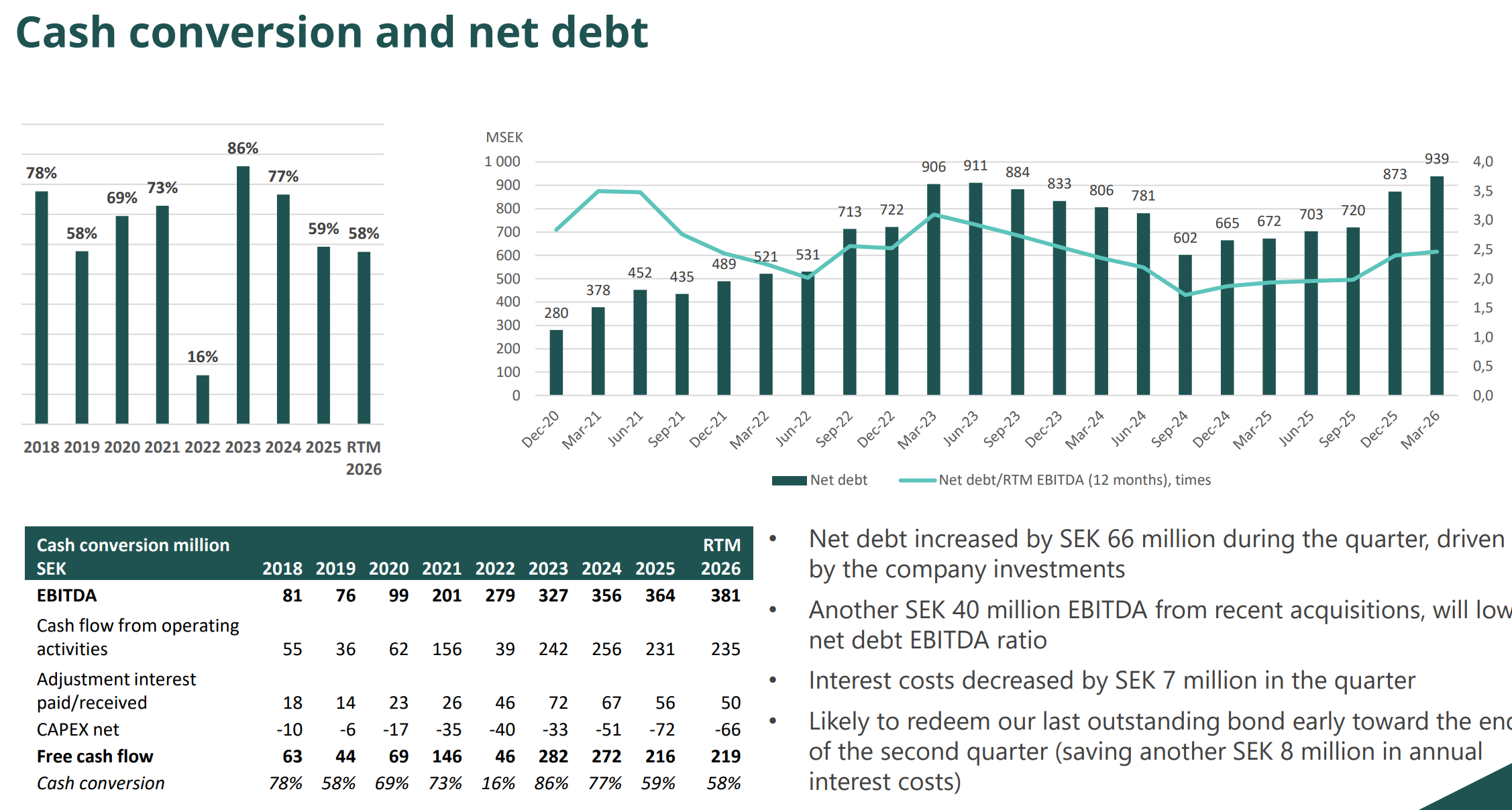

Idun reports under K3 accounting rather than IFRS, which means goodwill is amortised rather than impairment-tested, suppressing reported EBIT and net income; EBITA is therefore the more useful metric, and the effective tax rate appears higher than Sweden’s 21% corporate rate because of the non-deductible goodwill charge. The business is relatively capital-light by industrial standards, with net capex of c.2.7% of sales and net operating working capital of c.18% of revenue, both broadly stable through the cycle, with much of the capex sitting in a grey area between maintenance and growth.

Idun’s net debt target is <3.5x, with net debt at Q1 2026 of SEK 939mn, equivalent to c.2.6x run-rate attributable EBITDA once Idun’s c.83% ownership share is applied, since virtually all group net debt sits at parent level and is fully borne by ordinary shareholders.

A March 2025 refinancing replaced expensive bond financing with cheaper bank debt saving SEK 20mn per year, and the June 2026 bond redemption saves a further SEK 8mn, adding c.4% to EPS per Carnegie estimates. A further SEK 40mn of annualised EBITA from recent deals not yet fully in the LTM brings run-rate group EBITA to c.SEK 370mn. After applying the attributable ownership share and the bond redemption saving, run-rate attributable FCF is c.SEK 200mn, equivalent to a c.5.3% FCF yield at SEK 330. Idun retains the great majority of this for reinvestment, paying a dividend of a maximum 10% of adjusted profit, currently SEK 1.15 per share.

How Idun Gets to 15% Growth

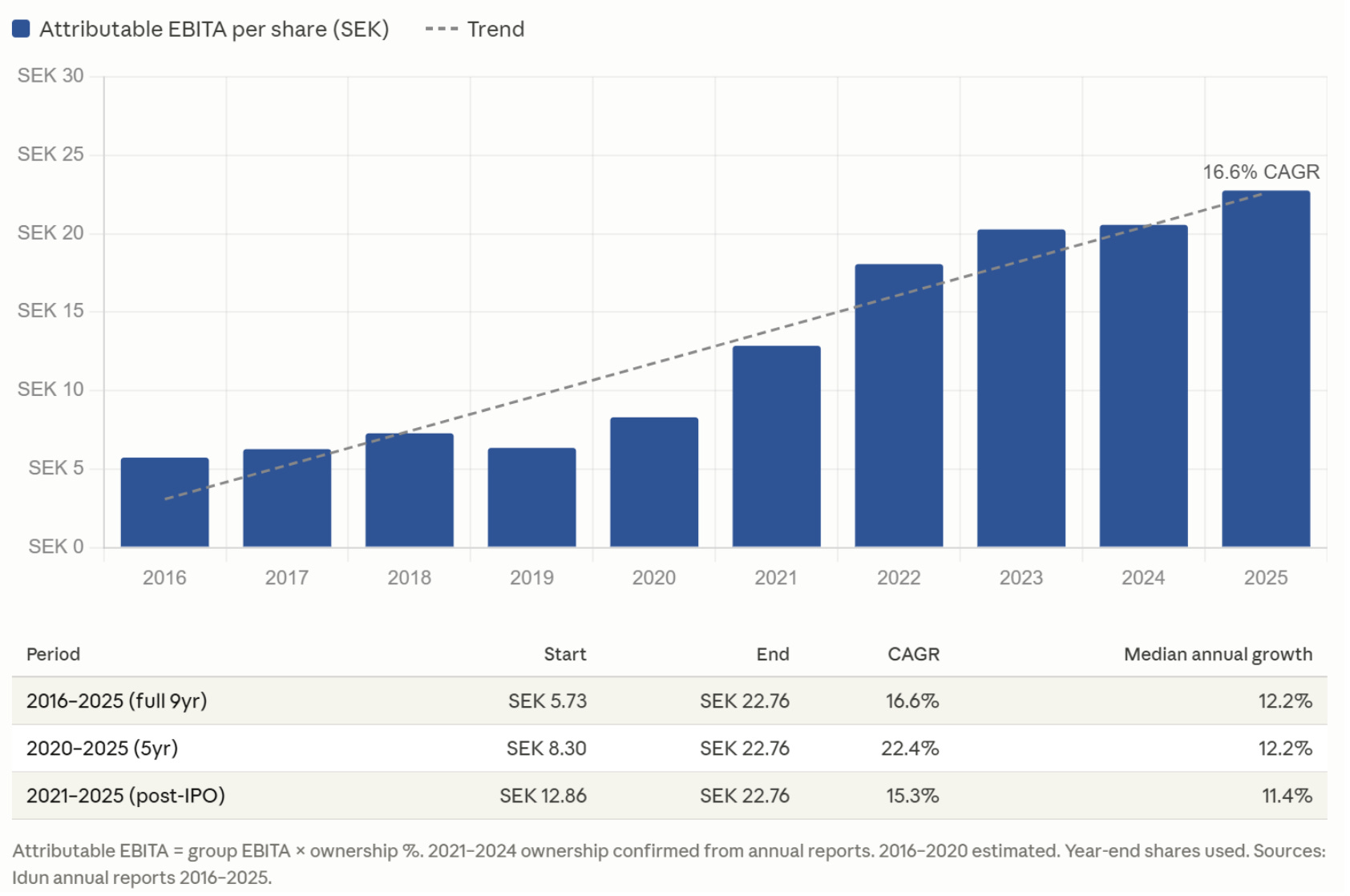

Idun's target is 15% annual EBITA growth, split 5% organic and 10% from acquisitions. Over nine years they have compounded attributable EBITA per share at 16.6%. Both engines have worked through the cycle, although not uniformly in every year, as the charts below show.

The math should work like this, in theory: On a run-rate basis the group generates c.SEK 200mn of equity free cash flow after interest and minorities, of which c.93% is reinvested after the dividend. Deployed at 5-8x EBITA, that implies pre-tax returns of 12-20% on incremental capital, and with 5% organic growth on top the combined engine should deliver the 15% EBITA growth target over the cycle.

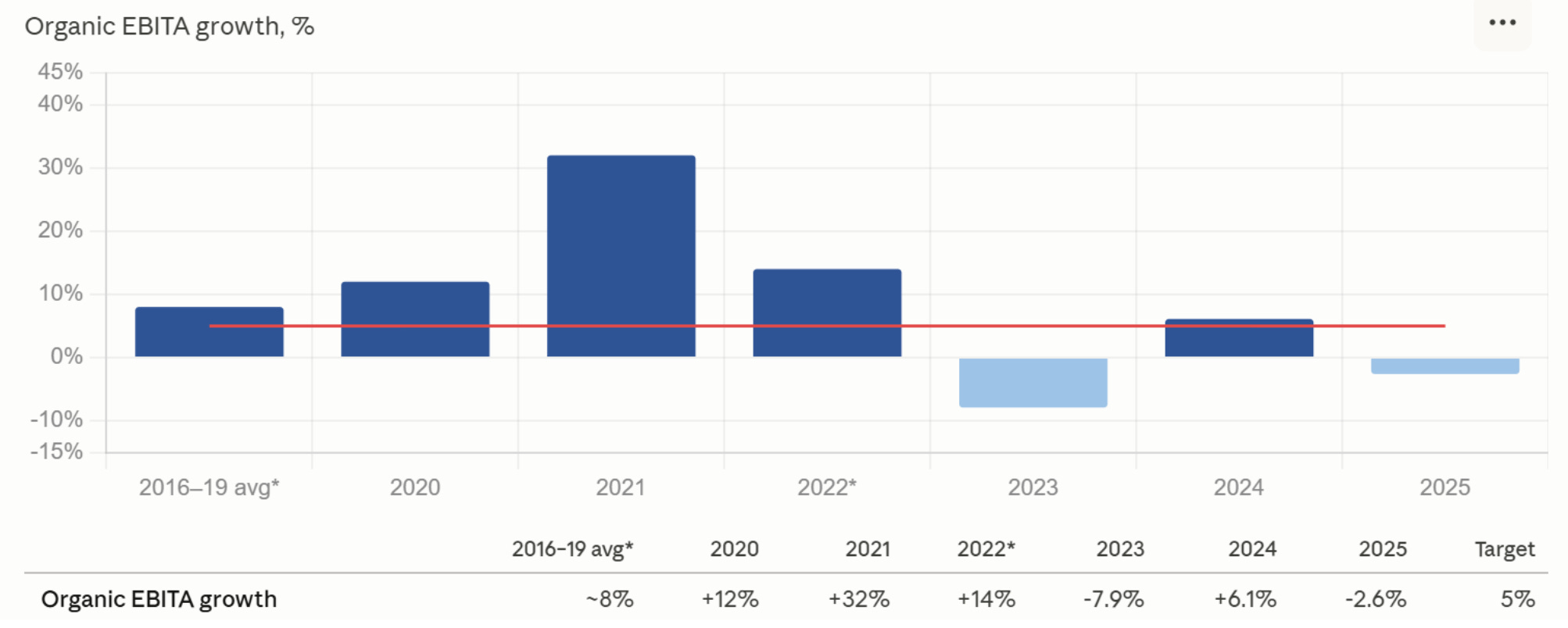

The Organic Story

The total EBITA number at Idun has held up in recent years because acquisitions have more than offset the organic weakness, which is how the model is designed to work, but the organic line matters because it tells you whether the underlying businesses are healthy

The organic chart above tells the story clearly. Through 2020-22, the engine ran well above target, averaging c.19% across the three years as operating leverage kicked in on a fixed overhead base during a strong industrial cycle. Organic EBITA growth turned negative in 2023 at -7.9% and again in 2025 at -2.6%, dragged down by customers in pulp and paper, heavy industry and process maintenance deferring spend.

The central question for investors is whether this is cyclical or structural. Gross margins held stable at c.60% throughout the downturn, which is the clearest signal available that competitive position has not deteriorated, as structural deterioration would show up in gross margin compression before it reaches EBITA. The demand deferral argument is equally credible: machinery wears out and deferred work cannot be ignored indefinitely, least of all in Ståthöga, Triton and P&L Nordic where scheduled maintenance eventually has to happen. The average organic EBITA growth over the full history since inception is c.8%, comfortably above the 5% target.

It is worth being precise about the portfolio’s cyclical exposure, since not all of Idun’s businesses were affected equally. The manufacturing segment, which accounts for c.60% of revenue, carries more cyclical exposure through Intermercato’s machine attachments and Culina’s commercial kitchen equipment. The service and maintenance segment at 40% of revenue also contains significant cyclical exposure, most notably through Ståthöga MA Teknik, the group’s largest single cyclical business at c.9% of group revenue, which provides heavy industrial maintenance and fabrication services to paper mills, steel mills and process industry customers. When those customers deferred maintenance through 2023-25, Ståthöga’s EBITA margin compressed from c.17% in 2024 to c.10% in 2025 on lower revenue, and that single business was a substantial contributor to the group’s organic earnings decline, with correspondingly significant recovery upside. Both segments also contain genuinely defensive businesses: EKAB and Prowash’s car wash operations in service and maintenance, and Fredahl Rydéns’ funeral products in manufacturing.

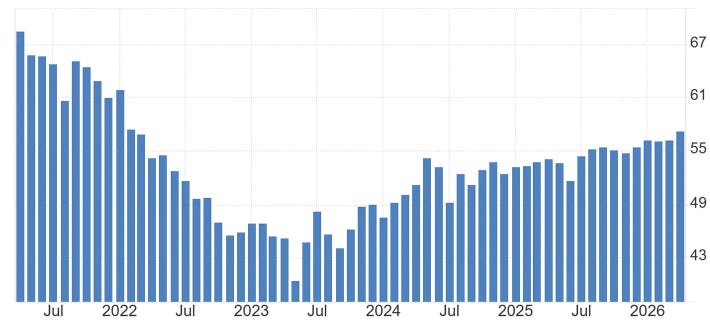

The macro data is now supportive: Sweden’s Swedbank Manufacturing PMI rose to 57.2 in April 2026 from 56.2 in March, extending its run above the long-term average for a tenth straight month and reaching its highest reading since February 2022.

Q1 2026 provided the first hard evidence of recovery in the portfolio itself, with organic revenue growth of 5% and organic EBITA growth of 1%, modest but in the right direction, and management guided that Q2 should be stronger. When the cycle turns, incremental margins should be high as the overhead base is relatively fixed.

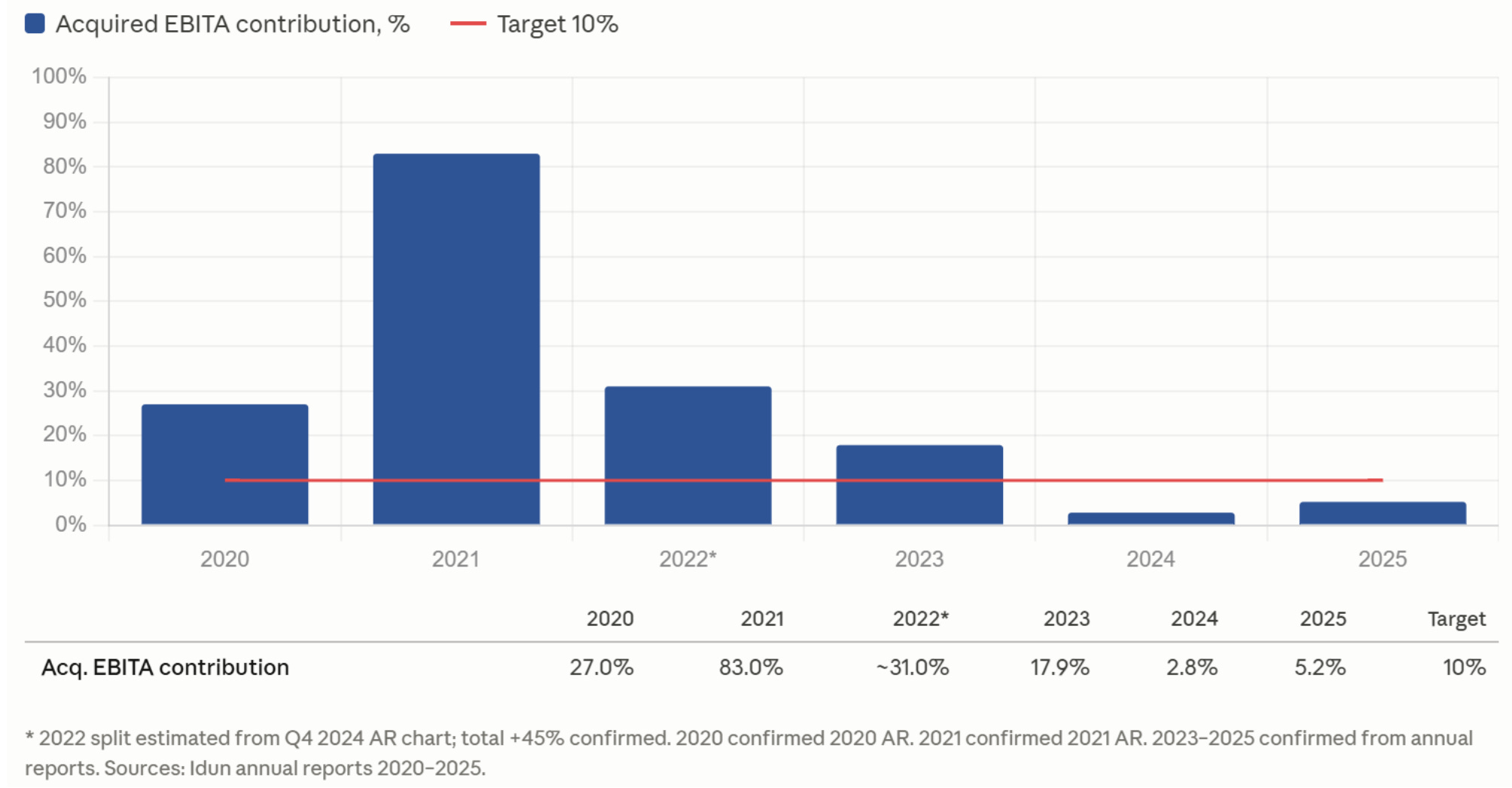

The Acquisition Story

The acquisition contribution has been more volatile, as the chart shows. The 2021 spike to 83% reflects five platform acquisitions in a single year funded by the IPO raise and two bond issuances, an exceptional deployment year that should be read as an outlier rather than a benchmark. The five-year rolling ROIIC of 16.1% confirms that capital deployed at 5-8x EBITA has generated returns comfortably above the cost of capital.

Acquired EBITA contribution was only 2.8% in 2024 and 5.2% in 2025, well below the 10% target, reflecting a deliberate decision to moderate the deployment pace as the industrial cycle weakened and balance sheet discipline took priority. With the March 2025 refinancing complete, headline leverage at c.2.4x EBITDA, and the pipeline active including the AGB deal announced in May 2026, the deployment rate should normalise through the year. Stegaföretagen’s own acquisition pipeline provides a further source of compounding that does not require Idun to deploy capital directly.

The attributable EBITA per share chart captures the combined effect of organic growth, acquisition deployment, ownership changes and share issuances in a single line. From SEK 5.73 in 2016 to SEK 22.76 in 2025, the CAGR is 16.6%, marginally above the 15% target on a per share basis over the full nine-year period.

Can Idun Hit 15% Growth Going Forward?

Q1 2026 came in at +16.8% total EBITA growth, with acquisitions doing most of the heavy lifting and organic beginning to contribute. The late 2025 and early 2026 acquisitions together added c.SEK 40mn of run-rate EBITA not yet fully reflected in reported numbers, and management guided Q2 stronger than Q1. Full year 2026 at or above 15% looks achievable, which would be the first year at or above target since 2022.

The underlying math for the longer term is straightforward. Internal cash generation of c.SEK 185mn per year after minorities and the dividend, combined with the SEK 450mn RCF and growing debt capacity as the group compounds at current leverage targets, is sufficient to fund the c.SEK 160-250mn of annual acquisition spend implied by the 10% acquired EBITA target at 5-8x multiples.

The honest caveat is that 15% will not come every year, and the organic component will be above target in strong industrial years and below it in weak ones, as the data above shows clearly. The question is whether the through-cycle average of 8% organic and the acquisition deployment of recent years is a fair guide to the next decade, or whether the early years of heavy IPO-funded acquisition spending flatters the historical number. On balance I think the model is intact, but investors should stress-test their own assumptions rather than take the historical CAGR at face value.

What the track record demonstrates is that the through-cycle average has met or exceeded the target: a business that compounds attributable EBITA per share at 16.6% over nine years through a pandemic, an industrial boom, a Nordic manufacturing recession and a rate cycle, while holding margins and balance sheet discipline throughout, has earned the right to be taken seriously on the 15% question but it is no guarantee they will necessarily meet it in the future. Over the medium-term, the upswing from here could be quite significant, as deferred organic growth returns and acquisitions resume at a normalised pace.

Capital Allocation

Serial acquirers live and die by the quality of their capital allocation. Storskogen, the other serial acquirer that listed in Sweden in 2021, which deployed capital at an unsustainable pace in 2021-22, acquiring poor quality companies and ultimately destroying shareholder value, is the cautionary tale. The best operators share a clear acquisition criteria they rarely deviate from, an aversion to overpaying, and an ability to maintain and grow businesses organically after acquisition.

Carnegie calculate that Idun has acquired companies at an average EV/EBITA multiple of 7.5x since the IPO, in line with the stated 5-8x range. In roughly half of those deals the transaction included the real estate used in operations, which typically attracts a higher multiple, meaning the implied multiple on the operating business alone is lower and day-one returns are therefore higher than they appear. The ROIIC calculation also requires adjustment for the unconditional shareholder contributions that Idun uses to inject equity capital into subsidiaries, SEK 130mn in 2025 and SEK 59mn in 2024, which represent real capital deployed but do not appear on the acquisitions line in the cash flow statement.

A few caveats before drawing conclusions from these numbers. The ROIIC includes organic EBITA growth in the numerator, which modestly overstates pure acquisition returns, though peers like Lifco and Lagercrantz are analysed on the same basis so comparisons hold. All figures are pre-tax, consistent with how serial acquirers are conventionally presented. Idun is also a younger group, meaning a larger share of the capital base reflects recent acquisitions that have not yet had time to compound. The five-year rolling ROIIC of 16.1% as of 2025 is the most meaningful single number, smoothing through the front-loaded 2021-22 deployment and the subsequent organic trough, and it has been remarkably stable.

One nuance worth flagging is the effect of minority buydowns. When Idun increases its stake in an existing subsidiary, the incremental EBITA flowing to shareholders goes up without any new operating capital being deployed into the business. It is arguably the highest-quality use of capital available to them: buying earnings they already know intimately, at a pre-agreed price, with no execution risk. The attributable EBITA share currently stands at c.83%, up from c.78% in 2020-23, and should drift higher as more minority buyouts are executed over time.

Idun is actively looking at acquisitions in other Nordic countries for the first time, and the team has appetite for geographic expansion beyond Sweden.

Idun’s capital allocation record to date is good. The path from good to great runs through continued discipline as the pipeline broadens geographically, the organic engine proves itself through a full recovery, and the returns on the existing capital base compound as the businesses acquired in recent years begin to mature.

Valuation

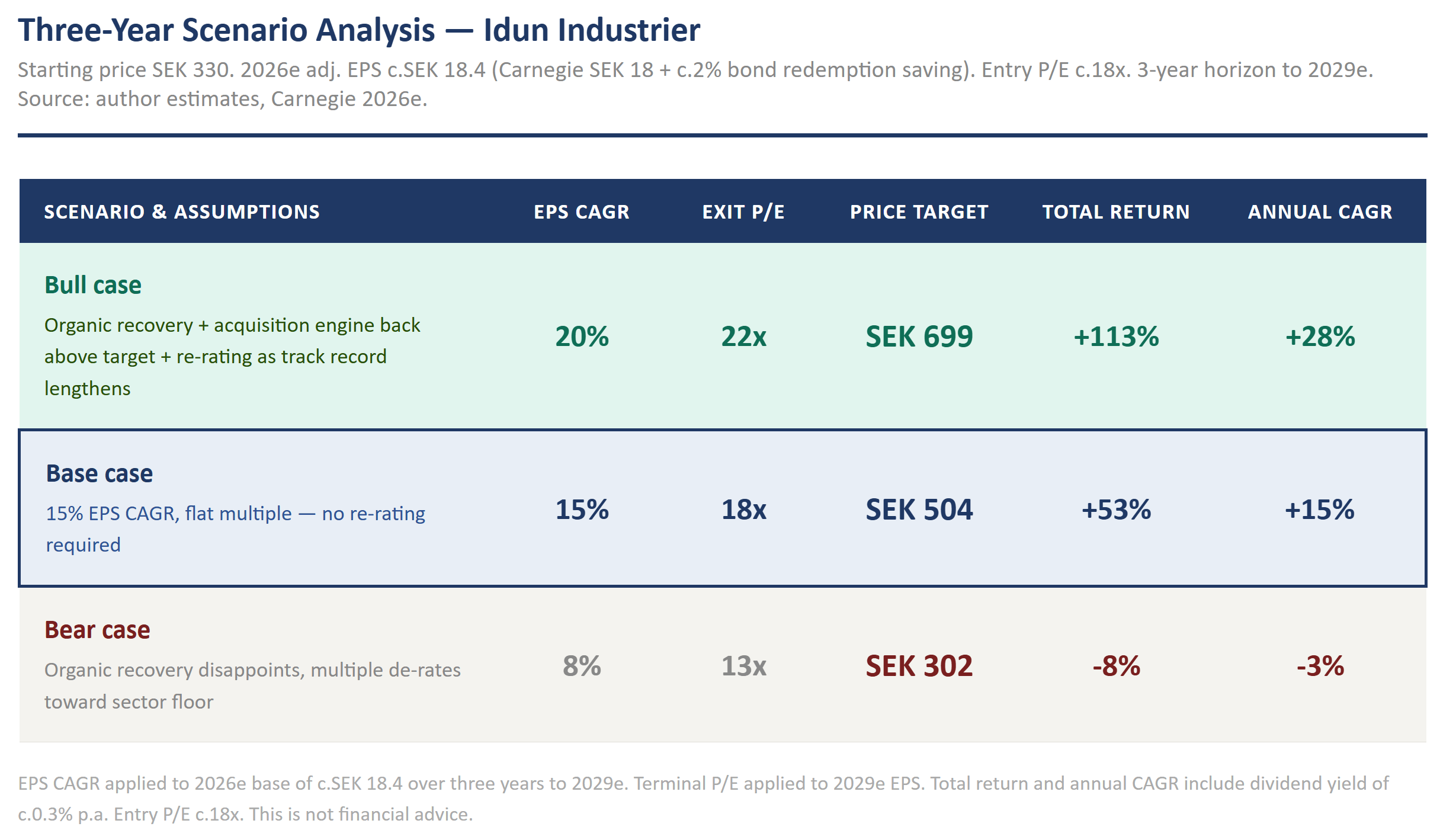

If the capital allocation record is a guide to what comes next, the valuation question becomes straightforward: is the entry price reasonable enough to generate an attractive return? At SEK 330 the entry is reasonable, although not overly cheap.

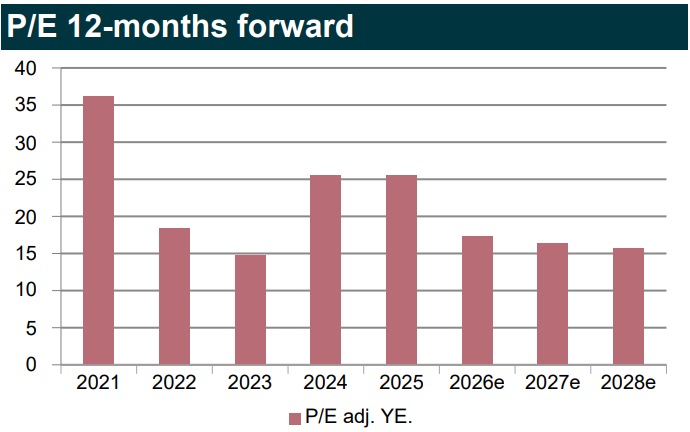

On an attributable basis, which is the right lens given the debt sits entirely at parent level and is fully borne by Idun shareholders, the business trades at c.16x run-rate EV/attributable EBITA and c.13x run-rate EV/attributable EBITDA as of Q1 2026. On a last twelve month basis those multiples are c.17x and c.15x respectively, reflecting the fact that several late 2025 acquisitions have their capital in the denominator but their full earnings not yet in the numerator. The adjusted P/E on Carnegie’s 2026 estimates, accounting for the interest cost saving from the bond redemption not yet in consensus, is c.18x, and the FCF yield on a run-rate attributable basis is 5.3%.

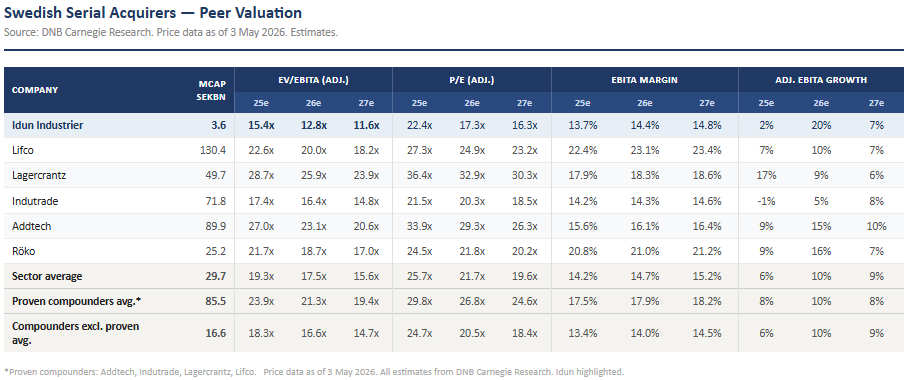

A note on reconciling these figures to the Carnegie peer valuation table published on 3 May 2026. Carnegie shows Idun at 12.8x 2026e EV/EBITA at their reference price of c.SEK 312 (implied from their market cap of SEK 3,592mn). At SEK 330, Carnegie’s 2026e EV/EBITA would be c.13.4x. The difference between this and the c.16x run-rate attributable figure above is explained by Carnegie using total group EBITA (100% of the group), while this piece uses attributable EBITA (c.83%), consistent with the fact that all of Idun’s net debt is borne by ordinary shareholders. Adjusting Carnegie’s 13.4x to an attributable basis gets to a c.16x multiple.

Against the peer group the discount is clear. Based on Carnegie’s numbers, the proven compounder average (Addtech, Indutrade, Lagercrantz, Lifco) trades at 21.3x 2026e EV/EBITA, and Röko at 18.7x. Idun at c.13-14x on the Carnegie total EBITA basis, or c.16x on an attributable run-rate basis, sits at the cheaper end of the peer group. Some discount is justified: Idun is younger, smaller and less liquid than Lifco or Lagercrantz, its organic growth has been more variable through the cycle, and its acquisition pace has been less metronomic, with deliberate slowdowns in 2023-25. None of these are structural criticisms but they are legitimate reasons for a valuation haircut relative to businesses with longer and more consistent track records.

The question is whether the current discount overcompensates for those differences. Over a full cycle the organic EBITA growth average has been c.8% and the five-year rolling ROIIC sits at 16.1%. Attributable EBITA per share has compounded at 16.6% since 2016, a strong track record achieved through a more challenging macro backdrop and with a younger, smaller portfolio than most peers. Lifco, for context, has a revenue base more than 10x the size of Idun's today. As that track record lengthens and the cycle turns, multiple expansion towards the 20-25x P/E range is the potential direction of travel.

A simple scenario analysis illustrates the return potential. If Idun continues compounding at its historical rate and the multiple stays flat at today’s c.18x forward P/E, the stock should compound at 15% p.a. The upside case is interesting with operating leverage as the cycle recovers, above-target organic growth as deferred demand comes through, and a gradual re-rating above 20x as the track record lengthens and the stock gets discovered. The bear case, multiple de-rating to 13x on disappointing organic delivery, implies a slightly negative return. That asymmetry, with the upside materially larger than the downside, is what makes the risk-reward interesting.

My own view is that SEK 330 is a fair entry into a well-constructed compounder at a point in the cycle where earnings are temporarily depressed, not a screaming buy but a reasonable initiation or add. I take a Turtle Creek-type approach: own it as a core long-term holding with the awareness that better entry and exit points will come along. I would be a more aggressive buyer below SEK 300 and would look to trim above SEK 420 as the multiple approaches the upper end of the peer range. At SEK 330 I am happy to hold, leaning towards adding on weakness.

Catalysts

(1) The Cycle Turns: Q1 2026 showed 5% organic sales growth, the strongest Q1 on record, but one quarter is not a trend. The H1 2026 results on 19 August are the test of whether that inflection is genuine, and two consecutive quarters of positive organic EBITA growth could change the narrative, proving that the trough of 2023-25 was cyclical rather than any structural deterioration in the businesses.

(2) Re-Rating as Track Record Grows: Idun trades at a discount to larger, proven compounders. This is partly justified by a shorter track record and lower liquidity. As the group compounds through a full economic cycle and demonstrates that capital allocation discipline holds up across different macro environments, that discount should narrow. The Swedish serial acquirer model commands premium multiples once trust is established, and Idun is still in the process of establishing it.

(3) Discovery and Uplisting: Idun began reporting earnings calls in English in Q3 2025, a signal that management wants to broaden the investor base beyond its almost entirely Nordic shareholder register. More international interest, paired with a move to the Nasdaq Stockholm Main Market, which management have indicated is possible over time, would broaden the eligible investor universe meaningfully.

Risks

(1) The Cycle Does Not Turn: If Sweden’s industrial recovery stalls in 2026, the organic recovery thesis could be delayed. The acquisition programme would continue regardless, but delayed organic recovery would slow progress towards the 15% EBITA growth target.

(2) Acquisition Quality and Supply: The long-term thesis rests on Idun continuing to source high-quality businesses at 5-8x EBITA. Overpaying, lower-quality deal flow, or increased competition from other serial acquirers would erode returns over time.

(3) Leverage: Group ND/EBITDA is c.2.2x run-rate, c.2.6x on an attributable basis. Comfortably below the 3.5x ceiling, but worth monitoring given the acquisition programme is funded partly through debt capacity. Excess leverage could constrain the acquisition programme and increases sensitivity to a higher rate environment.

(4) Key Person Risk: Eight people run the parent company. The loss of Adam Samuelsson or Henrik Mella, or other key personnel would be materially disruptive. The incentive structures that make departure unlikely are also the main mitigation.

(5) Controlling Shareholder: Adam Samuelsson controls 79% of the votes through Class A shares. Though the structure is in many ways more a feature than a bug, the dual class structure limits the prospect of a takeover bid and may preclude some institutional investors on governance grounds.

Conclusion

Having done the full work on Idun, the picture that emerges is of a business that is temporarily under-earning against a genuine long-term compounding track record. The portfolio quality is good rather than exceptional in aggregate. What is exceptional, and genuinely rare at this market cap, is the management alignment: a pedigreed team running a permanent capital vehicle where their wealth compounds through the share price alongside any outside shareholder, supported by 100 or so co-owners across the group companies, some of whom have taken personal loans to buy stakes in the businesses they run.

The thesis is straightforward enough. Idun is under-earning because Sweden’s industrial cycle is near a trough and the acquisition engine has been deliberately run below capacity while management prioritised the balance sheet. Both of those things are temporary. When the cycle turns, the combination of organic operating leverage, a normalising acquisition pace, and a track record that lengthens with each passing year should produce several years of above-target compounding. At SEK 330, with a 5.3% FCF yield, I am comfortable holding and would add meaningfully on any weakness below SEK 300. The businesses are good, the capital allocation has been good, and the alignment is exceptional. Whether Idun becomes the next great Swedish serial acquirer remains to be seen, but the foundations are as good as I have seen at this stage of the journey.

Disclaimer: This is not financial advice and only for informational purposes. I hold a position in Idun Industrier. Do your own research.

Sources: Idun Annual Reports 2018-2025; Q1 2026 Interim Report; Q1-Q4 2025 Earnings Calls; Redeye Serial Acquirers Conference 2026; DNB Carnegie commissioned research; Swedish company register (Bolagsverket) and Allabolag.se for subsidiary revenue and margin data. All figures SEK unless stated. Images copyright Idun Industrier AB.

For further reading: Paul Dutz wrote a good overview piece on Idun in 2024. Carnegie produce commissioned research on the company. REQ Capital, shareholders in Idun, have written extensively on Swedish serial acquirers and are worth reading for broader context on the asset class.

I also like Idun, and have followed them a while. I am looking to buy it around 300. One last thing I need to get past before I can pull the trigger however.

Do you have any thoughts about the quite substantial dilution which occurred in 2024? Shares outstanding went from 10.6 to 11.5 million. Directly before the dilution, the CIO sold 1/4 of his stake. The timing was not a good look, and I initially viewed the stock as a no-go for me. However, I do like the shareholder alignment in general.

Curious as to your thoughts. Thanks.

Thank you, interesting article. I like your investment idea, especially the management alignment with shareholders is great to see. I might be interested in buying at lower prices myself. Currently there are some other options with potential higher upside out there, that’s the only regret with the setup for me.