Whitbread (WTB LN): Checking Out of Restaurants, Checking Into Returns Focus

FY26 Results and Strategic Reset: Shedding restaurants, cutting CAPEX and management shifting to a returns focus. Moving towards a pure-play. Right steps, execution risk remains, Corvex lurking.

Better Plan, Now Down to Execution

Whitbread is not the type of business I would normally invest in but the activist involvement here caught my eye. Capital allocation has been poor, underlying earnings growth has been so-so, the UK hospitality environment is genuinely difficult, and management have just abandoned one five-year plan after 18 months. The stock is down 30% over the last five years, near-term earnings momentum is weak and sentiment is at a low ebb. That said, this week’s announcements are worth paying attention to. Pushed by an activist, management seem more open minded and have taken real and uncomfortable steps to reset the business to become a leaner, more pure-play hotel operator: exiting food and beverage, cutting gross CAPEX by £1bn, recycling £1.5bn of property, cutting 3,800 jobs, and shifting from growth-at-any-cost to a returns focus. This is a management team trying to regain credibility and they are under big pressure now to deliver this plan with the activist investor, Corvex, present on the register.

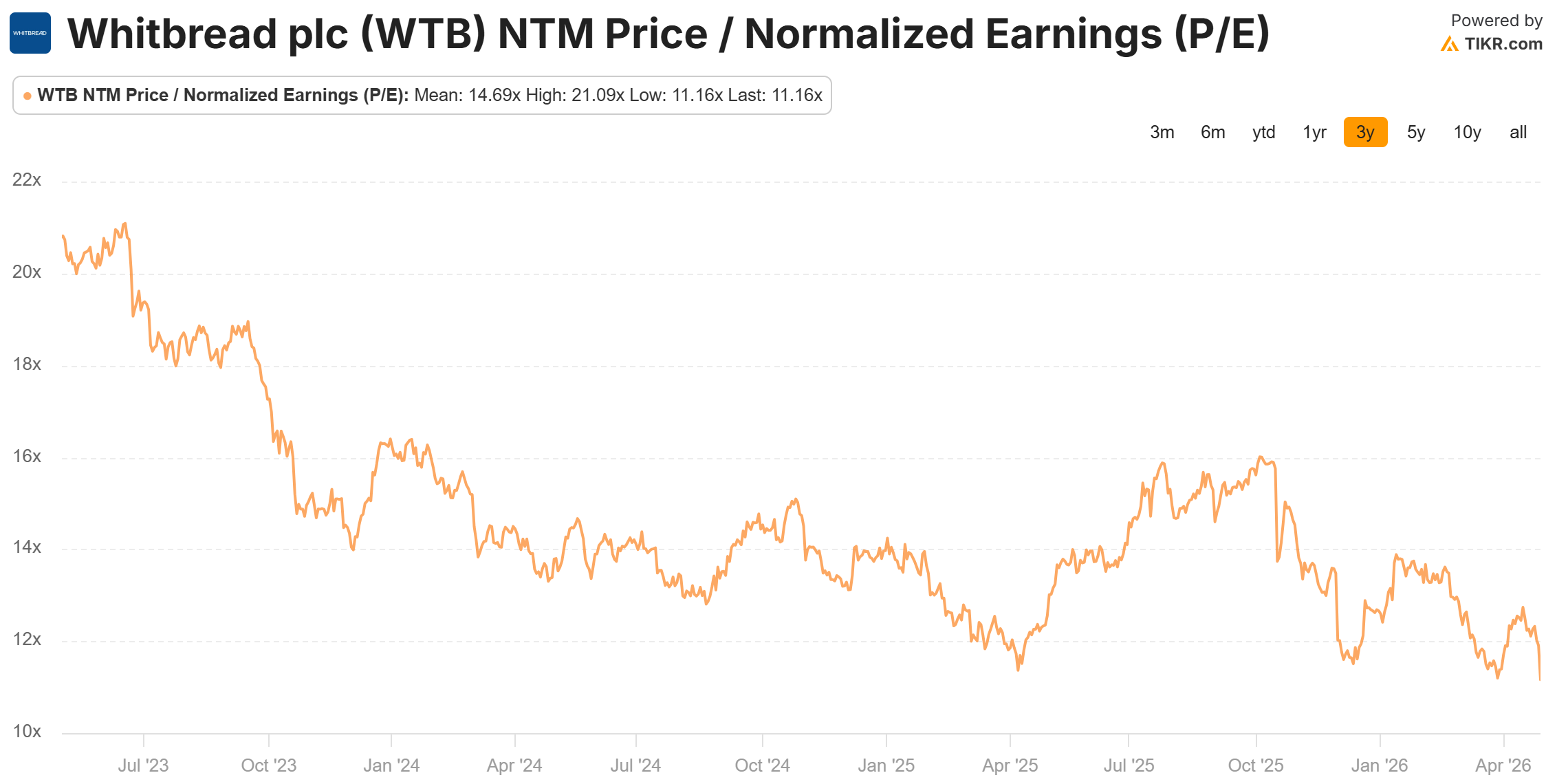

The stock is cheap on normalised cash flow, the property floor limits the downside, and the right tail is interesting. Feels like sentiment is close to a bottom after yesterday’s earnings downgrades. If the market still fails to rerate after delivery, Corvex has every incentive to push for something more radical. I think this is a reasonably cheap entry (£22 SP, <12x earnings), with bombed out sentiment, an activist backstop, and structural optionality. I’ve taken a small tracking position.

This ship will take a while to turn and I’m not in a rush to take a meaningful position here as this plan is a five-year story. I'd need to see early signs of delivery before pressing the position further. Execution was the problem with the last plan and it remains the key risk here.

A Reluctant Reset: Better Tone, Abandoned Targets, Capital Allocation Finally Improving

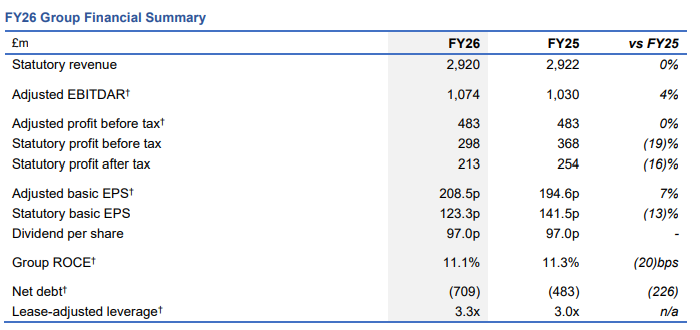

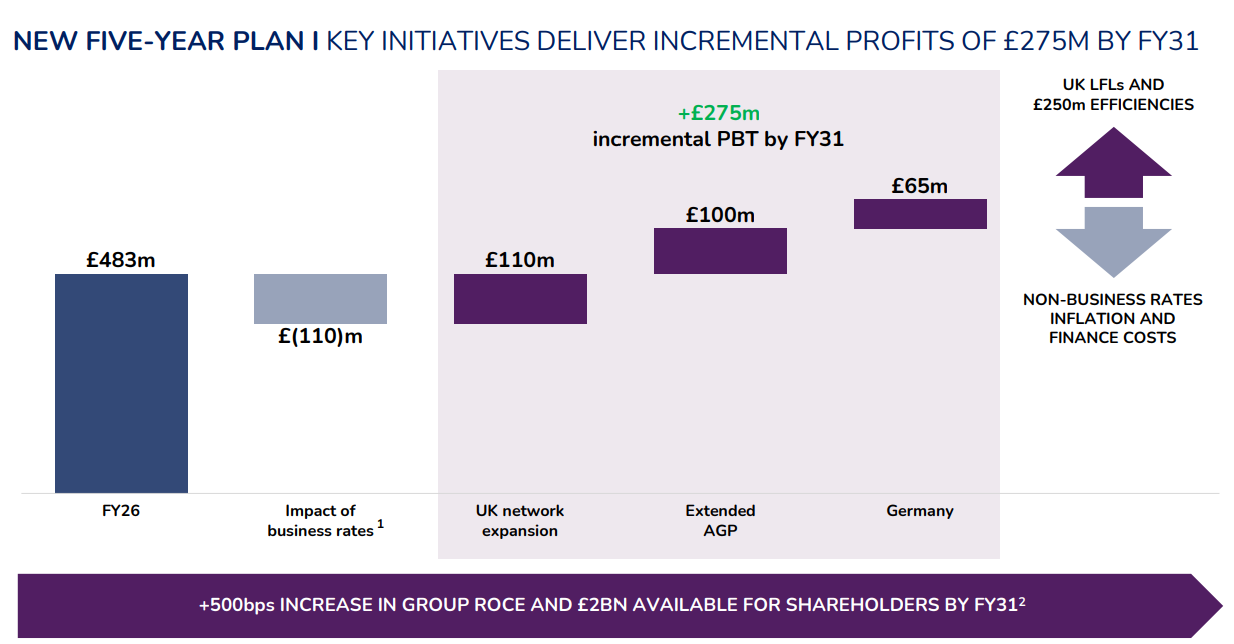

The stock fell over 6% yesterday on the day of announcement. The sell-off was driven by the FY27 earnings downgrade that wasn’t fully baked in by sell-side consensus. Headwinds from business rates, the Accelerated Growth Plan extension, inflation at the top of the guided range, and a £5mn hit from the Middle Eastern JV hurt FY27 guidance. Buybacks have also been paused. Some brokers had flagged this but consensus had not come down enough and the market sold the stock on this. I thought that the market might look through this more, or have already incorporated it, but the stock sold off on the earnings downgrade with the strategic reset an afterthought. FY26 itself was decent: adjusted PBT flat at £483m despite real cost headwinds, Germany profitable for the first time at £2m, cost efficiencies beat at £83m, and UK RevPAR outperformed the market.

The management tone was noticeably candid. CEO Dominic Paul acknowledged on the call that Germany was run with a UK mindset from the start and that they overpaid for some sites that do not fit the model as it has evolved. That level of honesty is refreshing. The broader acknowledgement that capital allocation has not been returns-led and that the FY30 plan is being scrapped after 18 months was overdue. The new plan runs to FY31.

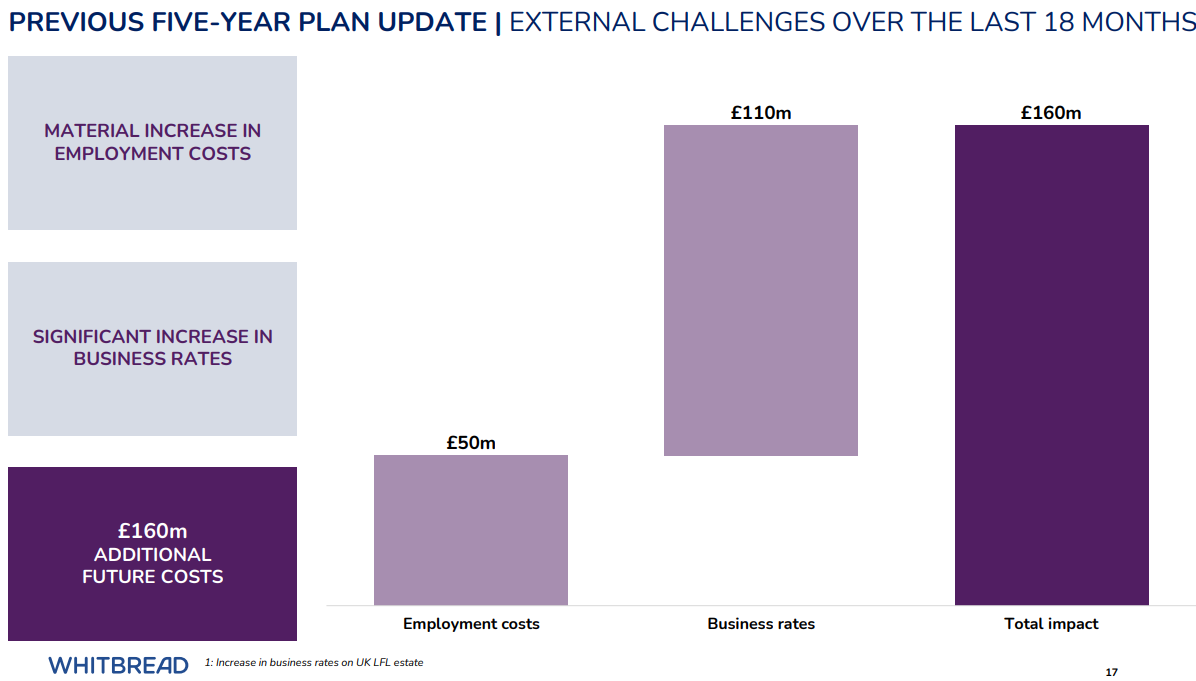

In fairness, management have been genuinely unlucky in places. The UK government reaching for business rates and national insurance to plug the fiscal hole was a material and largely unpredictable headwind that changed the economics of projects that were viable under the prior plan:

“It is fair to say that the last two UK budgets have not been kind to the hospitality sector... taken together, these factors have hit the whole hospitality industry hard. For us, before mitigation, they are expected to reduce future profits by around £160m.” — Dominic Paul, CEO

At the same time, Whitbread management have created enough of their own problems. They over-invested in expansion, chasing growth for the sake of it at the expense of returns. Germany was underperforming before business rates were an issue and the prior expansion programme was too aggressive regardless. Some of this reset is clearly Corvex-driven. The activist took a 6% stake in December 2025 pushing for exactly this, a reduction in the property discount and more disciplined capital allocation. Corvex have not made money here and will keep the pressure on. The question is whether management can execute a second plan having failed to deliver the first. If they cannot, board representation is the logical next step for Corvex.

The most significant shift is from growth and market share towards returns on capital. UK room growth targets are reduced, pipeline projects below hurdle rates have been exited, and the Germany room target has been cut from 20,000 to 18,000 rooms. Dorchester is the clearest example, planning consent had been secured but the site is now being sold because business rates pushed the return below internal hurdles. The CEO was explicit on the call that this is no longer about chasing a growth target for the sake of it.

The Plan: Exit Restaurants, Cut CAPEX, Recycle Property & German Improvement

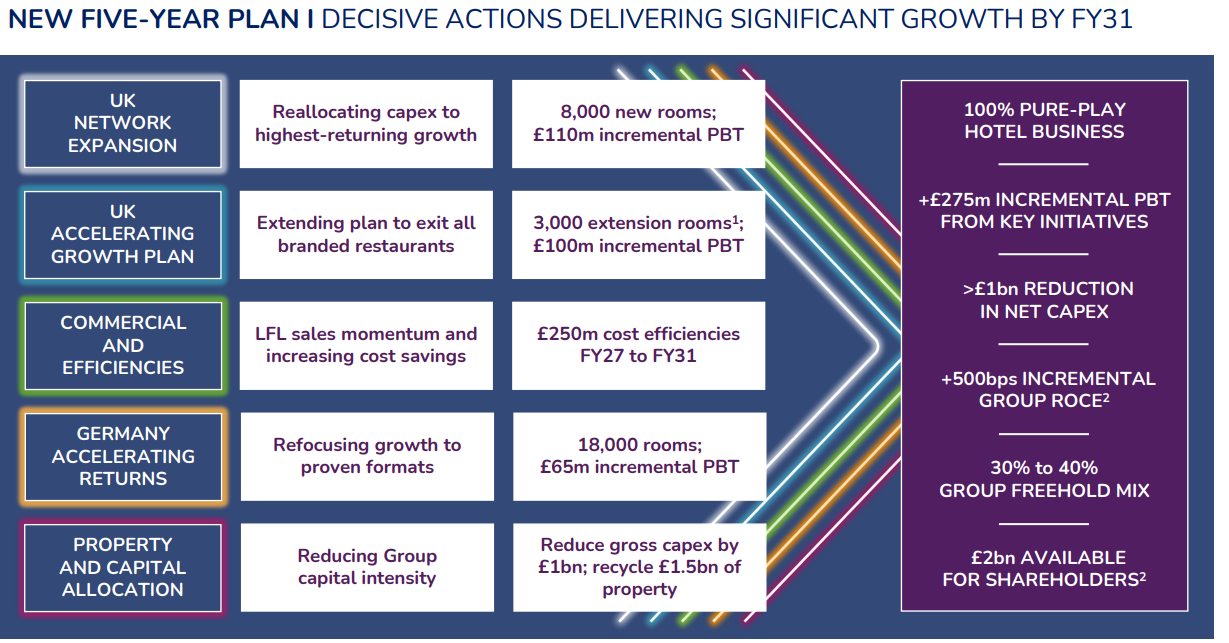

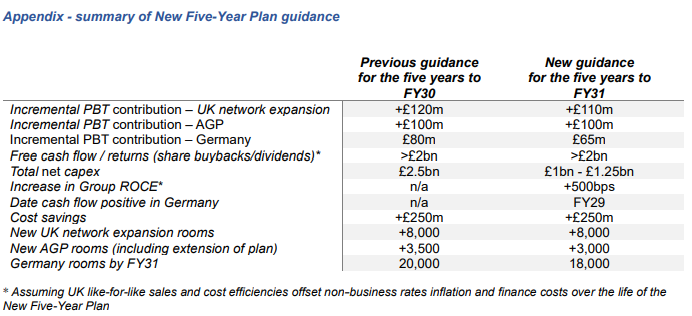

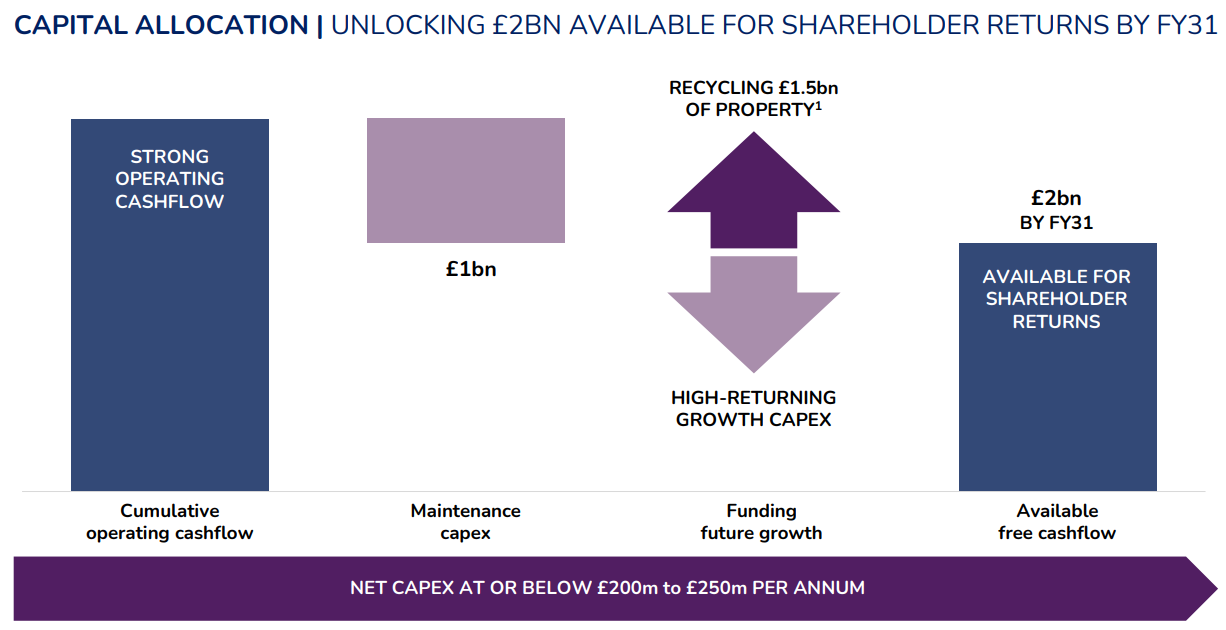

So what does the updated plan actually look like? The headline numbers are: £1bn gross CAPEX reduction over five years, £1.5bn of freehold property recycled, net CAPEX at £200-250m per annum versus £500m previously, freehold ownership falling from 50% to 30-40%, £275m of incremental PBT targeted by FY31, and a 500bps ROCE improvement to around 16%.

The most operationally significant decision is extending the Accelerating Growth Plan to cover all remaining 197 branded restaurants. These currently generate £284m of food and beverage revenue but run at a site-level adjusted loss of £13m before tax, plus £10m of central overheads. Management are converting 87 into hotel extension rooms and selling or closing the remaining 110 over the next two years, involving around 3,800 job losses, a direct consequence of UK government policy making the operation uneconomic. The transition hits FY27 profits by a net £10m and the full £100m incremental PBT benefit is not seen until FY31. Simon Ewins put the economic logic plainly:

“The average margin across our 500 integrated sites is around 10 percentage points higher than it is for sites served with a branded restaurant.” — Simon Ewins, MD UK Operations

On property recycling, the net CAPEX reduction is the most important financial change in this plan. Gross CAPEX falls by £1bn over five years, but more importantly net CAPEX drops from around £500m per annum to £200-250m, funded by recycling £1.5bn of freehold property. That halving of net capital intensity is what drives the step-up in free cash flow and shareholder returns over the life of the plan. Management sell mature freeholds at 5-6% yields and redeploy into the AGP at guided 15-20% returns. The spread is attractive if it comes through. Most shareholders would probably prefer the proceeds back via buybacks rather than trust management to redeploy at those rates given the track record, but if the AGP delivers what management expect the redeployment is likely accretive. The capital return story is back-end loaded: no buybacks in FY27, Germany cash flow positive by FY29, and the full £2bn shareholder return target not reached until FY31.

Germany is the part of the plan that requires the most faith. The business turned profitable for the first time in FY26 at £2m of PBT, with Hamburg already delivering double-digit site-level returns, and management now have a clearer view of what works, larger city centre hotels in the right locations. The room target has been cut from 20,000 to 18,000 and all future growth will be funded via leaseholds or property recycling. Encouraging progress, but brand awareness sits at 19% in Germany versus over 90% in the UK and the journey to profitability took far longer than expected. There is a lot of execution risk and it remains to be seen what returns on capital the >£1bn German investment will ultimately deliver.

Low Expectations… Worth Tracking Execution

UK hospitality is not a sector you would generally seek out. Roughly six businesses are closing per day in 2026. But the activist involvement, the reset, and the valuation together create a situation worth paying attention to. There is genuine turnaround and re-rating potential here if management execute, with the property estate providing a floor on the downside.

On normalised cash flow, stripping out expansion CAPEX and assuming the plan broadly delivers, the stock looks cheap relative to the current market cap. That yield improves significantly, well into the teens, as the AGP completes, Germany matures, and the cost programmes work through. There are three things to watch closely for over the next 12 months: (i) the disposal yield holding near the FY26 level of 5.4% on £450-500m of guided FY27 proceeds, (ii) early AGP site performance as more completions come through, and (iii) any signal from Corvex on whether they are satisfied or pushing harder. If those are moving in the right direction by the interim results, the case for building gets considerably stronger.

The risk-reward looks more interesting than it has for some time. Earnings downgrades are out of the way, sentiment is at a low ebb, and the right tail is genuinely interesting. If management execute and the market still fails to rerate, Corvex has every incentive to push for something more radical. At this price relative to asset value and the stock’s own history, the case for a more fundamental review only grows stronger the longer the discount persists. The business is becoming simpler and easier to underwrite, a cleaner candidate for some form of transaction if the new strategy does not close the gap.

The key risk is the same as it was with the last plan, execution. That is why I have taken a small tracking position, watching closely.

Note: This post is for informational purposes only and does not constitute investment advice. I may hold positions in securities mentioned. Always do your own research before making any investment decision.

If you found this useful, consider subscribing to The Value Junkie for more ideas and analysis.

Charts and data

1. Group financial summary

2. Summary of New Five-Year Plan Guidance

3. External Challenges

4. Capital Allocation

5. Key Initiatives to FY31

British Property Billionaire Richard Livingstone ($5.3bn net worth per Forbes) takes a 3.5% stake in Whitbread.

He also bought a similar sized stake in October 2022 when sentiment was at a low (c. +30% return for WTB over the next year). Richard is a property developer who jointly the privately held London & Regional Properties alongside his brother.

Thank you for sharing your two articles. I have not been tracking Whitbread as closely in recent months, so getting an update was useful.

That said, it remains unclear to me how Whitbread can be anything other than a "value" story - through re-rating and/or property disposals - which, ironically, has an even less favourable IRR if you think even the new plan is a "five year story". Buffett said time is the friend of good businesses and the enemy of bad ones, and Whitbread seems distinctly in the latter category.