Whitbread (WTB LN): An Interesting Activist Situation

Activist-driven strategic review highlights potential to unlock value, with a shift toward a capital-light model as a key lever. Management will update market alongside FY26 prelims on April 30th.

I was recently asked to identify an interesting situation in European equities over the next six months and landed on Whitbread for the reasons below. I wrote this up last week and am sharing it now, updated for the Sunday Times article that landed on April 25th which, if accurate, confirms the direction of travel. This is not necessarily a recommendation, just sharing my work on the company with the wider community.

The Setup

The market has punished Whitbread for a combination of poor capital allocation, a weak UK trading environment and rising costs. Business rates following the Autumn Budget added a £35m annual headwind from FY27. NIC increases and labour inflation compound the pressure. RevPAR was negative for six consecutive quarters before a partial recovery in Q3 FY26. The five-year FY30 plan set in 2024 is being reset after 18 months and Germany, the long-term growth story, is only turning profitable now. The stock currently trades at just over £24, close to its five-year low and the stock price has gone backwards over the last five years. (Image Source: Google Finance)

The result is a company trading at a c.£4.6bn EV against an independently verified property portfolio worth c.£6bn, meaning the market is ascribing zero to negative value to the operating business. That operating business is Premier Inn, the dominant UK budget hotel operator with 86,000 rooms and approximately 40% of the UK branded budget segment. This dislocation attracted Corvex Management, a proven activist, which took a 6% stake in December 2025 and has publicly forced management to reassess their Five-Year Plan, including the £3.5bn investment programme.

The downside is anchored by the property floor. The upside is a forced capital allocation reset, with a hard public deadline of April 30th.

Background

Whitbread (WTB LN) is a FTSE 100 hospitality company and the owner and operator of Premier Inn, the UK’s largest budget hotel chain with over 86,000 rooms across more than 800 hotels. It also has a growing presence of over 11,000 rooms in Germany. Once a sprawling conglomerate with interests in Pizza Hut, Costa Coffee and Stella Artois, it has spent the last decade simplifying into a focused hotel business.

What makes Whitbread an anomaly in the global hotel industry is its ownership model. The modern hotel playbook, adopted by Marriott, Hilton, IHG and Accor, is asset light: these groups franchise or manage hotels owned by third parties, collecting fees without tying up capital in property.

Whitbread never made that journey. It owns 51% of the hotel rooms it operates, sitting on a property portfolio independently valued at up to £6.4bn. That asset has been hiding in plain sight for years, and the SOTP argument has long been discussed. The reason it has never fully re-rated on this basis is straightforward: structural value that cannot be unlocked is theoretical value. A company sitting on a property portfolio worth more than its market cap is interesting, but not necessarily actionable if management has no intention of doing anything about it. The SOTP has historically been a framework that showed the discount without providing a reason for it to close.

What has changed is Corvex. The presence of a credible, well-resourced activist with 6% of the company and a public position on the property discount transforms the previously theoretical into something that now has a realistic path to realisation. April 30th is the first hard test of whether that path is opening.

Who is Corvex?

Corvex Management is a New York-based activist hedge fund founded in 2010 by Keith Meister, who spent years as a key lieutenant to Carl Icahn before striking out on his own. The fund manages approximately $3bn and runs a concentrated, fundamentally-driven book with a longer-term investment horizon than most activists. Meister’s approach is less table-thumping than some of his peers: he prefers to engage constructively with boards and management teams, treating activism as a last resort rather than a first move.

His track record of forcing structural change and unlocking value at companies with complex capital structures is well established. He pushed for management changes at CenturyLink, partnered with Icahn to force the sale of Energen Corporation, and has repeatedly targeted situations where he believes the market is undervaluing assets trapped by poor structure or capital allocation. The fact that Corvex chose Whitbread, a UK-listed company outside its usual hunting ground, and took a 6% stake with a public letter calling out the property discount, signals serious conviction and intent to follow through.

Catalyst: April 30th, Three in One

FY26 results, an updated strategy, and rebased FY30 targets all land simultaneously on April 30th. This is a rare convergence of catalysts.

The base case is CAPEX rationalisation, reset targets, and accelerated sale and leaseback transactions beyond current guidance. The January 2026 LondonMetric transaction (£89m across 9 sites at a 5.3% NIY) confirmed the sale and leaseback programme works beyond prime London assets.

A full PropCo/OpCo split is operationally complex and unlikely on the day, but cannot be ruled out given Corvex’s public position on the property discount. The CEO committed on the January earnings call to reviewing “all options.”

Update, Sunday Times April 25th: Whitbread is expected to announce the sale and leaseback of one in five freehold properties it currently owns, releasing approximately £1.5bn for shareholders. This would reduce freehold ownership from roughly 50% to 40% of Premier Inn hotels, turning Whitbread into a majority leasehold business for the first time since Premier Inn was founded in 1987. Deutsche Numis described the April 30th announcement as “particularly important” while analysts at Morgan Stanley said the revised plan should “reassure investors.”

The stock reacted with a 3% gain on Monday morning following the article before retracing the move by the close. That is an interesting data point in itself. Either the market is treating it as just a rumour until confirmed on Thursday, or the scale of the strategic shift has not yet been fully absorbed. Either way, with the confirmed announcement two days away, the move has faded rather than been built upon.

Valuation: Two Frameworks, Same Conclusion (Roughly)

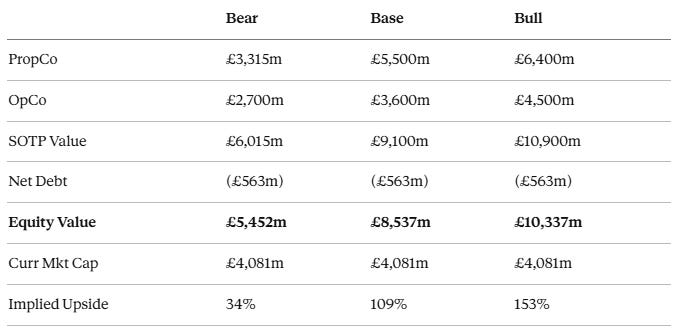

Sum-of-the-Parts (SOTP)

Separating Whitbread’s property and operating businesses:

The independently verified RICS portfolio is valued at £5.5bn to £6.4bn at yields of 5.5% to 6.5%. The OpCo, if it were to pay market rent on those properties, would earn approximately £400m of EBITDA (maybe more), which I value at 9x, reasonable for a dominant branded operator. Deducting net financial debt, SOTP fair value is c.£50 per share against a current price below £25.

As noted above, this SOTP has been visible to the market for some time without closing the gap. The difference now is that Corvex has latched onto the same framework and is actively pushing to make the theoretical real. That is what makes the timing of this interesting rather than just the valuation itself.

One genuine caveat worth flagging: the RICS valuation reflects Whitbread as a strong, creditworthy tenant on a relatively modest rent burden. As more properties are sold and leased back, the total rent obligation grows, fixed charge cover deteriorates and subsequent buyers of freeholds may demand higher yields to compensate for a weaker covenant. In practice this means the first tranches of the S&LB programme clear at tighter yields (the LondonMetric deal at 5.3% NIY supports this) while later transactions may be done at 6.5% to 7% or wider. The programme has diminishing returns at scale, and the aggregate proceeds are unlikely to reach the top of the RICS range. The base case is probably the right anchor rather than the bull.

Traditional Multiples

Even rejecting the SOTP framework, Whitbread trades at 8.5x EV/EBITDA and 12x P/E against five-year pre-pandemic averages of 10x and 16x respectively. Both frameworks point to the same conclusion: Whitbread is undervalued relative to the latent value trapped by its current structure, which is now being addressed.

As Corvex stated plainly in December 2025, the current share price appears to ascribe no value to Whitbread’s UK operated leasehold portfolio, its German hotel assets, or its development properties under construction.

The Short Position and Why It’s Interesting

WTB is the fifth most shorted stock in the UK, with 9.2% of the float disclosed short according to ShortTracker. Names include Marshall Wace, Millennium, Citadel, D.E. Shaw and Two Sigma. A who’s who of multi-strategy pods, not tourists.

The shorts are probably focused on near-term earnings risk into April 30th. Given these managers have the resources they do and focus on these events they may well be right that Whitbread is under near-term earnings pressure. The EPS headwinds are real and well documented: the £35m business rates hit in FY27 rising under transitional relief over three years, NIC and labour inflation, and the ongoing German drag. Sell-side numbers have been coming down, and it is likely consensus has not yet fully caught up with where updated buyside expectations have settled, which could pose guidance risk on the day. The shorts could be right on earnings, and I am not going to argue otherwise.

Where it gets interesting is whether April 30th reframes the conversation entirely, away from near-term EPS and toward structural value realisation. The thesis here is not that earnings are great. It is that there is significant value trapped in the structure of this business that Corvex is pushing hard to unlock. If management delivers something credible on April 30th, the question shifts from “when does EPS recover?” to “how much capital gets returned and when?” which could change the narrative.

Risks and Mitigants

(i) Management disappoints on April 30th Delivers only incremental changes with no structural commitment. Mitigant: the stock is already mispriced on a standalone property basis, and Corvex with 6% would be expected to escalate.

(ii) Near-term EPS pressure Business rates £35m FY27 headwind increasing under transitional relief over three years, plus NIC and labour inflation. Mitigant: Whitbread has a strong track record of cost delivery (c.£80m in FY26), though full offset over the three-year transition is not assumed.

(iii) Sale and leaseback at scale creates permanent rent costs and diminishing returns Later transactions in the programme may happen at materially wider yields as the covenant weakens, reducing aggregate proceeds below headline RICS-implied values. Mitigant: £1bn+ of Group EBITDAR with rent cover intact, and the value unlock remains significant even at wider yields on later tranches.

(iv) Weak UK economy and consumer RevPAR recovery depends on supply continuing to tighten. A weaker-than-expected UK economy could delay or reverse this. Mitigant: structural supply dynamics from independent hotel closures and below pre-COVID supply levels provide a tailwind independent of demand.

(v) Germany continues to drag The German business is only now profitable after years of capital consumption. A slower path to profitability would weigh on group earnings and capital allocation credibility. Mitigant: German RevPAR up 7% in Q3 FY26 and the business is on track to reach profitability this year.

(vi) Corvex has no confirmed board seat Mitigant: 6% stake, a public letter, a hard April 30th deadline, and Meister’s track record of escalation.

What to Watch

April 30th is the key date. A strategy reset, a move toward a more capital-light model, CAPEX rationalisation, meaningful capital returns and rebased targets would likely be taken well by the market. The interesting thing is that this combination does not yet appear to be catching the attention it probably deserves. April 30th may change that.

The question is whether management delivers something structural or merely incremental. A credible sale and leaseback programme and CAPEX rationalisation would likely reframe the investment case meaningfully. A same-as statement with no structural commitment would disappoint, though the property floor limits how far the stock can fall from here.

Corvex’s next move is the other thing worth watching. With 6% and a hard public deadline, the activist dynamic does not go away quietly regardless of what management delivers on the day.

This is not financial advice. Do your own due diligence.