Portfolio Update: July 2026

Three adds and an exit: buying the dip on the TerraVest controversy, IPO positioning at D'Ieteren, topping up Idun on a pullback, and a profitable checkout from Whitbread

July 2026 Portfolio Update

Welcome to the first of these portfolio updates. I write detailed pieces on individual companies, but a lot happens in between posts, so the idea here is to keep tabs on the names I have covered and own, along with any news that matters to the theses. This is a summary of the moves that seem worth mentioning rather than a log of every trade, and the intention is for it to become a regular note.

It has been a busier month than usual. I sold and then rebought some TerraVest around the insider trading story, added significantly to D'Ieteren, topped up Idun Industrier, and closed out my Whitbread tracker position at a profit. The details on each below.

TerraVest Industries (TVK. TO)

During the month I sold a decent clip of TerraVest around the C$158 level before buying it back, and then some, at an average of around C$108 after the insider trading press reports that I covered in more detail here. To summarise what happened: the story broke on the 5th of June that Quebec’s financial regulator, the AMF, alleges that executive chairman Charles Pellerin shared privileged information with nine family members and acquaintances ahead of the announcement of the EnTrans acquisition in March 2025. No charges have been filed, and the board, excluding Pellerin, commenced a formal review and stated it will cooperate fully with regulators. The stock fell c.32% on the news. It is a significant governance blow, but one that reflects no deterioration in the underlying business, which is why I was happy to add on the drop.

Since then there has been no update on the case and the stock has recovered to the C$118 level, which should be a good base to build on over the coming months as TerraVest continues to produce earnings growth and acquire more companies.

The controversy hasn’t stopped the acquisition machine either, as TerraVest announced last week that it has completed the bolt-on acquisition of Superior Pressure Vessels Inc., an Alberta-based manufacturer and service provider of pressurized transport tanks and trailers that will join TVK’s Compressed Gas Equipment division. It is a positive sign that the controversy did not prevent this seller from completing their transaction with TerraVest.

“Headquartered in Calgary, Alberta, SPV is a well-known manufacturer of pressurized tank trailers serving the Canadian market. The Company has a loyal brand following, a reputation for quality and has been in business for over 45 years.”

I continue to hold TerraVest. Sentiment has likely been close to a bottom, and the company is well placed to move on from this controversy, continue compounding earnings and trade better in the market over the medium term.

D’Ieteren (DIE BB)

I added significantly to my position during the month on a pullback at an average price of c. €165, for the reasons I set out in my original piece here.

The clear catalyst to unlock value here remains the potential Belron IPO. While there was little news on that front this month, the successful IPO of SpaceX, the largest listing in history and trading well above its offer price, should lead to more positive conversations in the boardroom on Rue du Mail in Brussels. A healthy IPO market bodes well for CD&R and Belron’s other private equity holders, who may well decide this is the right time to list Belron.

In the last week or so the stock has traded between the €174-€182 level. Where it trades short term is anyone’s guess, but the move back upwards likely reflects enthusiasm for a potential Belron IPO, which, if announced, could send the stock to levels upwards of €200. I am a content owner for now.

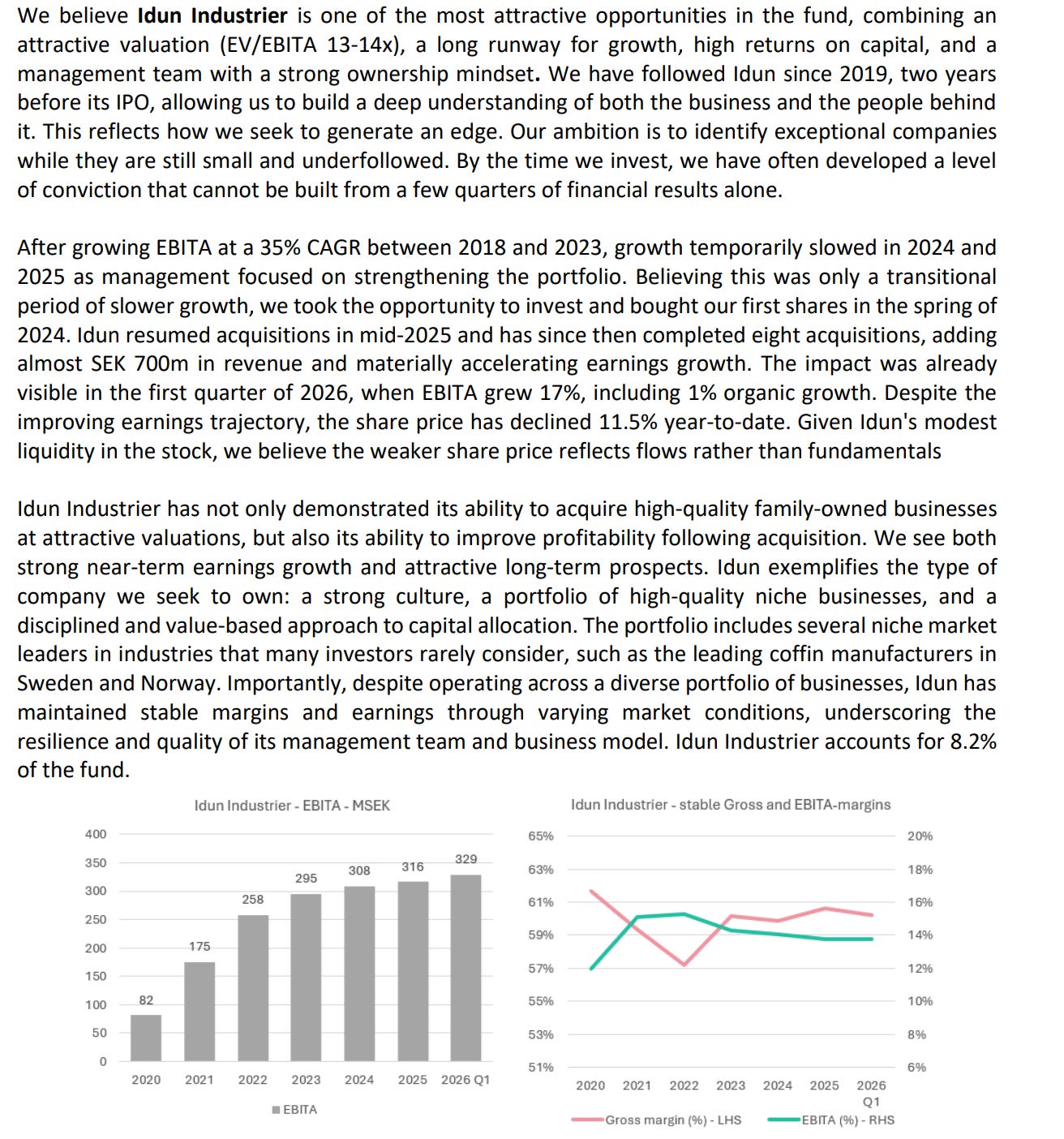

Idun Industrier (IDUN-B ST)

I added to my position in Idun Industrier just this week around the SEK 300 level. In my piece here I mentioned I would be willing to add closer to the SEK 300 level, from SEK 330 at the time of the post, and the market gave me that chance this week.

Operationally, Idun continue to execute their acquisition programme, announcing another acquisition on the 29th of June, acquiring 85% of the shares in Nordbergs Tekniska AB, a leading Swedish distributor of highly specialised technical and engineered polymer materials, serving customers in areas such as medical technology, defence, telecom and demanding industrial applications. Nordbergs was founded in 1970, has net sales of c. SEK 77mn with a reported EBITDA margin of c. 24%, and will report within Idun’s Manufacturing business area. The brothers Valdemar, Oskar and Pontus Nordberg will remain as shareholders, and everyone currently active in the company will continue in their operational roles. This is the classic Idun playbook, buying a dominant business in a specific, overlooked niche, with the people who built it left in place to keep running it.

“It feels good for the future to have Idun as a long-term ownership partner. We have built the company over many years and look forward to continuing to develop the business together with Idun, with the same focus on customer satisfaction, quality, service and fast deliveries as always,” says Valdemar Nordberg, CEO and shareholder of Nordbergs.

The acquisition is expected to have a marginal positive impact on Idun’s 2026 earnings, and is financed through a combination of own funds and existing credit facilities. Alongside the deal and the previously communicated early redemption of the company’s last outstanding bond of SEK 220mn, Idun has increased its revolving credit facility from SEK 450mn to SEK 670mn, which leaves plenty of financial flexibility for further deals from the pipeline.

The backdrop for Swedish small caps more broadly is worth a mention here. REQ Capital, shareholders in Idun, noted in a recent letter that the first half of the year saw a flow-driven rotation out of Swedish small and mid caps, largely driven by redemptions from Swedish funds, and that small caps now trade at a 9% discount to large caps against a historical average premium of 6%, a spread last seen around the financial crisis. In their experience these dislocations tend to be relatively short-lived, and when capital starts flowing back in, the door can quickly become crowded. Idun’s shareholder register is almost entirely Nordic, so it sits directly in the path of any reversal of those flows.

REQ, who are a leading voice in the Nordic Serial Acquirer space, wrote about Idun in their latest investor piece, linked here. I have attached the Idun portion here below.

Closed Position: Whitbread (WTB LN)

Whitbread was a tracker position I took in the wake of the extremely negative sentiment that followed their Capital Markets Day in late April, which I wrote about here. At the time of the post the stock was trading around £22. I sold my position into strength at £25.35 in late June, a c.15% gain in two months.

While there is potentially a lot of value at Whitbread, the mechanism to unlock it will take time, and there continue to be disagreements between the activist Corvex and the management team on how best to do it. Sentiment was bombed out, which made for an attractive entry, but there are too many outstanding questions for me to have the conviction necessary to increase the position and I preferred to invest elsewhere once the stock recovered, as Whitbread would not be the prototypical type of investment case for me. I will continue to track developments at Whitbread as an observer for now.

Disclaimer: This is not financial advice and only for informational purposes. I hold positions in TerraVest Industries, D’Ieteren and Idun Industrier. Do your own research.