D'Ieteren (DIE BB): The Belgian Holdco Hiding a World-Class Business at Half Price

80% of NAV sits in an exceptional business getting ready to go public, yet the stock trades at a 50% discount to NAV. The Belron IPO looks increasingly likely and D'Ieteren is the only way to play it.

D’Ieteren (DIE BB) | Share price: €172.40 | May 2026

Market Cap: ~€9.2bn | ADV: 73,200 shares/ €13mn | 53.7mn shares outstanding

Pitch

D’Ieteren is a Belgian holding company trading at a c.50% discount to my estimate of NAV, where 80% of that NAV is concentrated in a world-class business, Belron, that should IPO in the coming year or so. The IPO will drive a re-rating of D’Ieteren’s NAV and, I expect, a meaningful compression of the holding company discount as their largest asset becomes publicly liquid and impossible to ignore. This double play makes D’Ieteren a core position for me with a two-year probability weighted IRR of 21%. A world-class asset base at half price, with a family-controlled shareholder that has a history of returning cash via special dividends. I like the asymmetric set-up here into the potential Belron IPO event, heads I win, tails I don’t lose much.

History & Background

I have followed D’Ieteren for close to two years, having first done work on it around the time of the shareholder reorganisation and special dividend in late 2024. I thought it worth sharing now given there’s a clear catalyst on the horizon in the form of the mooted Belron IPO.

D’Ieteren is a seventh generation, family-controlled company that has been involved in the automotive industry and adjacent areas for over 220 years. As the Brussels Times highlighted: “Since 1805, the business has survived Napoleon’s march across Europe, Belgium’s independence revolution, two World Wars and, of course, the transformative arrival of the internal combustion engine.” The family business started when Jean-Joseph D’Ieteren began working as a coach-builder on the Rue du Marais in Brussels. The group entered what became its principal business, auto distribution, in 1931. Initially the group distributed US brands (none of which exist today) before getting its big break when it signed an agreement to import Volkswagen Group vehicles in 1948. In 1999, the group acquired what became by far its most impactful investment: Belron (50.3% ownership at present), the windscreen repair and replacement business. Since then, D’Ieteren has also added control or co-control stakes in TVH Parts (40%), an aftermarket parts distributor serving the material handling, construction, industrial and agricultural industries, PHE Europe (91%), a distributor of vehicle spare parts Western European countries, and in a departure from the group’s business services and light industrials focus, Moleskine (100%), the Italian lifestyle brand.

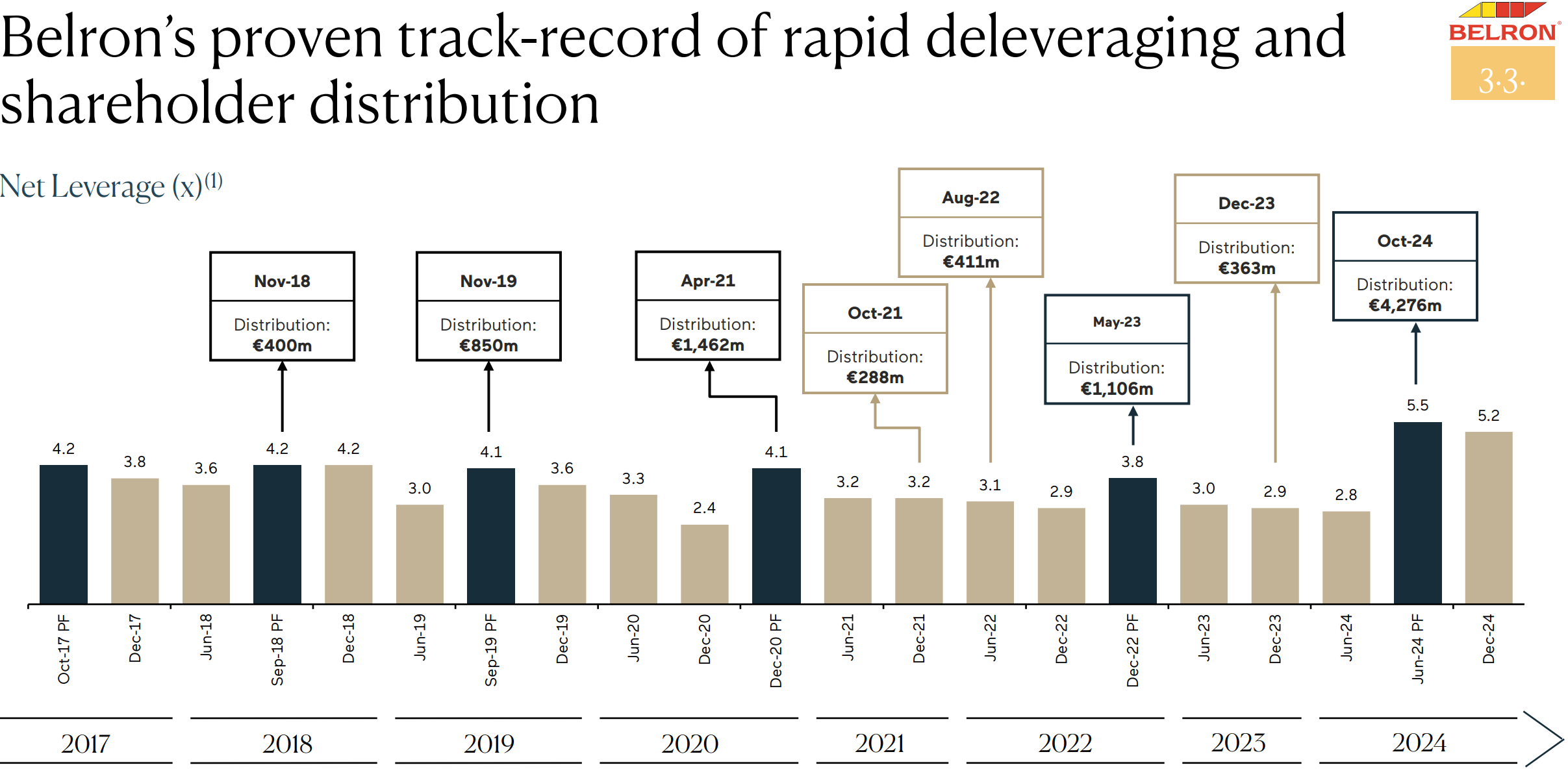

The business has been passed down the generations to its current owner Nicolas D’Ieteren, the second richest Belgian, whose net worth is substantially tied to his 50.1% stake in the group. Unlike many large family-controlled European companies, D’Ieteren has kept its shareholding consolidated along a single line rather than fragmenting across branches. This discipline was reinforced in 2024 when Nicolas bought out his cousin Olivier Périer, the former Deputy Chairman, in a transaction funded by a €4.3bn dividend recapitalisation at Belron. This helped fund a €4bn payout at the group level, including an exceptional dividend of €74 per share paid to all shareholders in December 2024. Nicolas’s family office Nayarit has increased its stake to 50.1%, while Olivier’s holding company SPDG Group has until 2029 to sell down its remaining 9.1% position.

Belron

Belron is the worldwide leader in Vehicle Glass Repair, Replacement and Recalibration (VGRRR) services. In 2024, Belron completed close to 17 million jobs across 40 countries, operating under more than ten major brands including Carglass, Safelite and Autoglass. It manages vehicle glass and other insurance claims on behalf of insurers, and operates through both a corporate business (North America, Western Europe and ANZ) and franchisees (typically in CEE, Africa and South America).

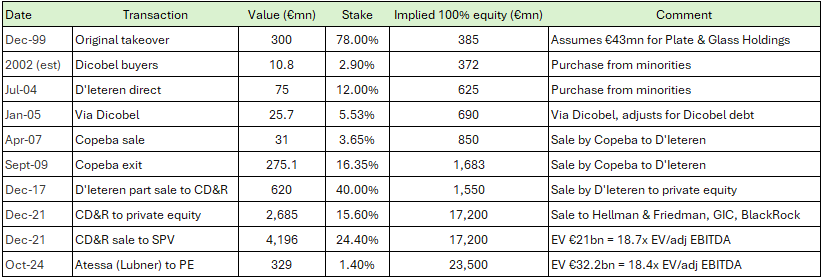

Belron was founded in New Zealand and has grown into the global leader in its category. Its US business, Safelite, accounts for approximately 55% of total group revenue and around 35% market share in North America, almost 10x the size of its nearest competitor. In some European markets, Belron accounts for close to two-thirds of the market. D’Ieteren first acquired a 68% stake in Belron in 1999 at an equity valuation of approximately €400mn. CD&R bought a 40% stake in 2018 at an enterprise value of €3bn, and sold roughly half of that to a consortium of Hellman & Friedman, GIC and BlackRock in 2021 at an EV of approximately €21bn (7x in four years). D’Ieteren currently own 50.3% of Belron.

Belron is led by CEO Carlos Brito, who took over in November 2022 having previously served as CEO of AB InBev from 2008 to 2021. He gave a good overview of the business at the 2025 Investor Day which is worth watching.

The Industry

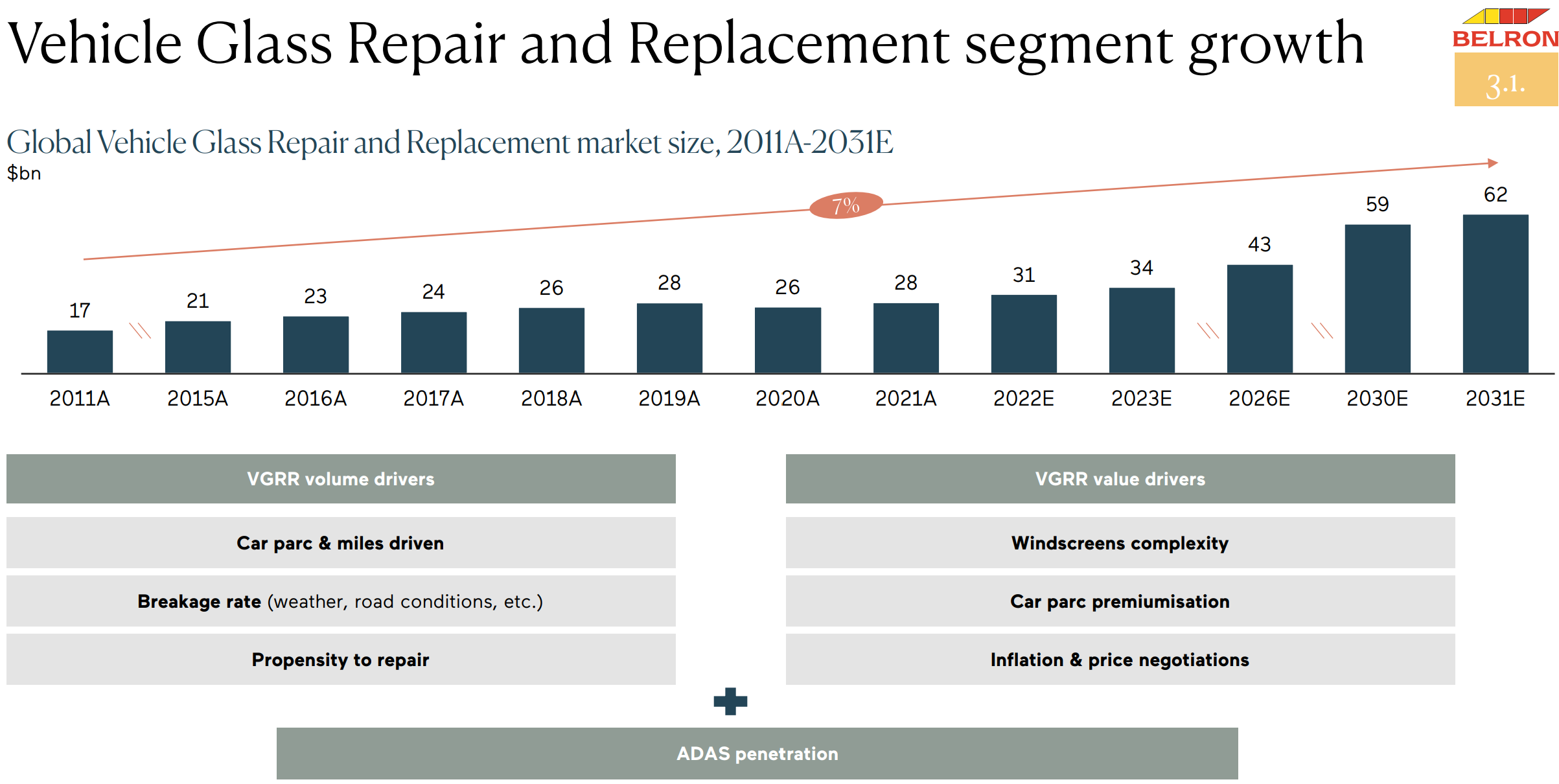

Repairing, or increasingly, recalibrating a damaged windscreen is as close to a non-discretionary expense imaginable given its paramount importance for driver safety. The VGRRR market is expected to grow at a 7% CAGR from 2011 to 2031, driven by both volume and value growth.

Volume growth is stable and growing slowly, driven by the size of the car parc, miles driven, breakage rates and the propensity to repair. Value growth is more clearly positive: windscreens are becoming more complex, an ageing car parc in the US and Europe will need to be replaced leading to premiumisation, and inflation and price negotiations with insurers all push average revenue per job higher. Over the past five years, Belron’s volumes increased at an annual rate of just 1.1%, while organic growth averaged 7.9% per year mainly related to the most powerful tailwind of Advanced Driver Assistance Systems (ADAS).

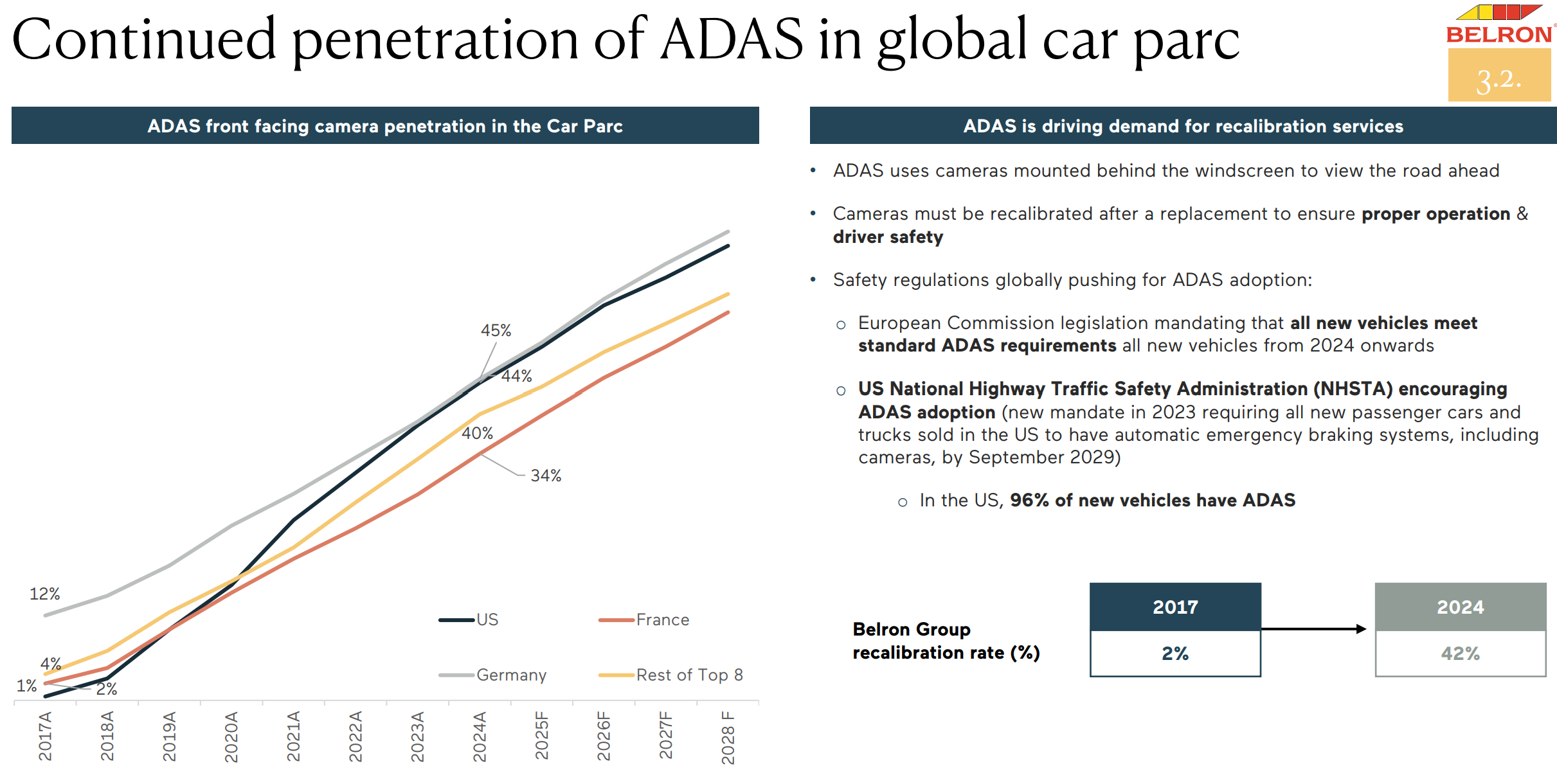

ADAS involves cameras, sensors and radar arrays typically mounted in or behind the windscreen, which require full recalibration whenever a windscreen is replaced. Belron’s recalibration rate has grown from just 2% in 2017 to approximately 47% of the cars for which they repaired or replaced the windshield for in 2025 and has increased at c.5% a year for the last decade or so. Critically, almost 40% of those vehicles that now require recalibration essentially did not exist before 2017. New cars are legally required to carry ADAS technology in both the US and Europe, so this penetration rate will only rise as the fleet turns over and Belron will be well placed to capitalise on this trend.

The Moat

Belron benefits from numerous competitive advantages as the dominant operator in almost all of its markets, with leading technical and service capabilities, economies of scale and the ‘friendly middleman’ dynamic of its relationship with car insurers being among the most important.

Scale is the foundation, Belron replaced over 17 million windscreens in 2024, making it the world’s largest purchaser of windscreen glass. This procurement scale gives Belron a material cost advantage that compounds, and a wider range of SKUs available allowing Belron to stock the right glass for virtually any car model within reach of their technicians. Beyond procurement, Belron has leading technical expertise in ADAS recalibration and glass technology that smaller operators can’t match.

The insurance relationship is an important structural advantage and the hardest to replicate. Around 70% of Belron’s revenue is generated from insured jobs, with the remaining 30% from fleet and leasing companies and cash-paying customers. Car insurers typically operate nationally and they prefer to contract nationally with Belron than to manage hundreds of independent operators. For many drivers, a windscreen replacement is their only insurance claim in any given year or number of years, despite paying significant annual premiums. Replacing a car windscreen is one of the few moments an insurer gets to proactively impress a customer by delivering a high-quality, efficient service and so insurers prioritise service and technical expertise rather than just focusing on price. Belron understands this and has always focused on delivering a quality experience for the driver. Belron is also tightly integrated into insurers’ IT systems. All 25 of the top US insurers use Belron for claims processing through their third party administration business with State Farm, the last holdout, having just switched over in the last year.

Financial Track Record & Outlook

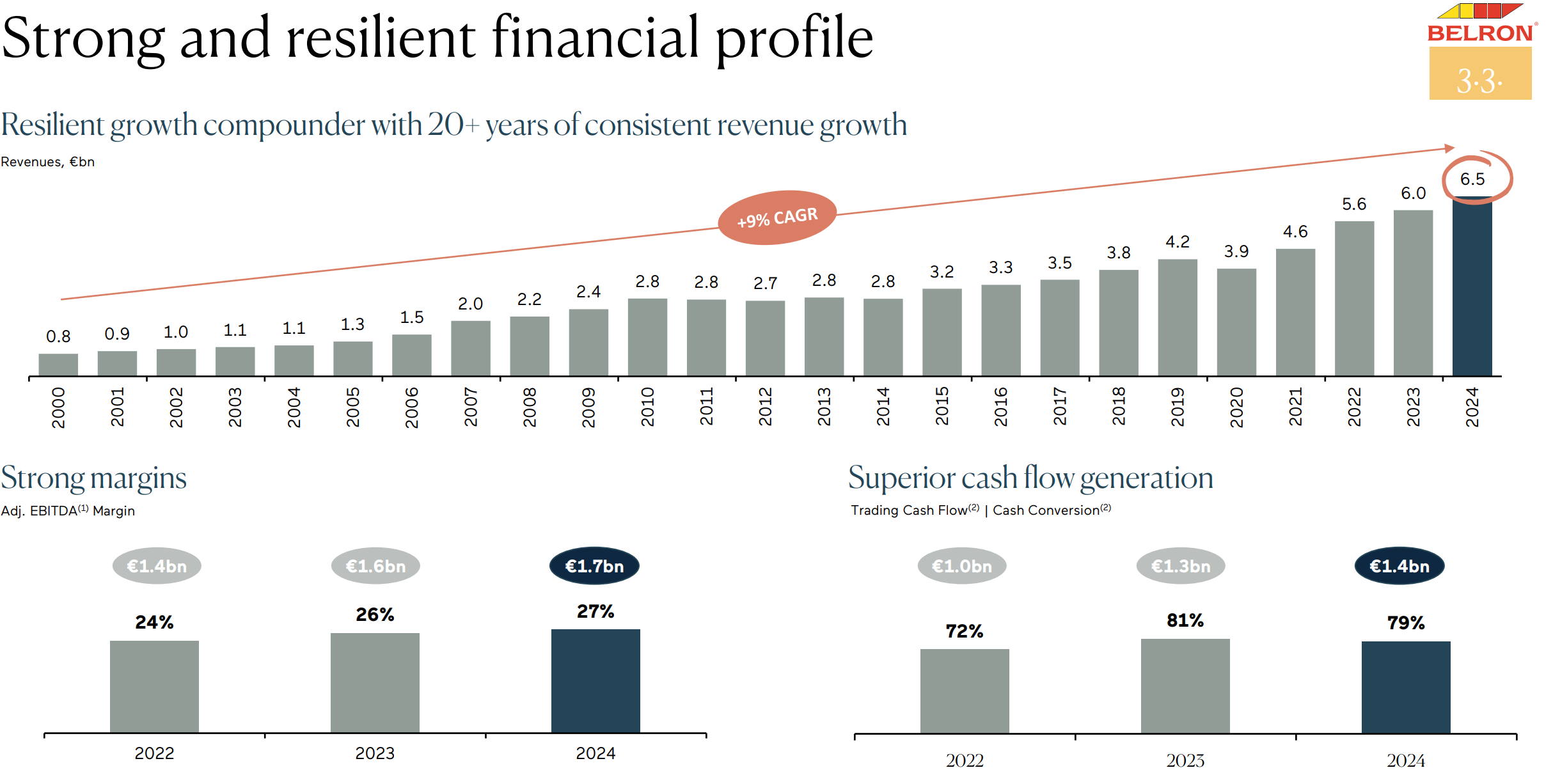

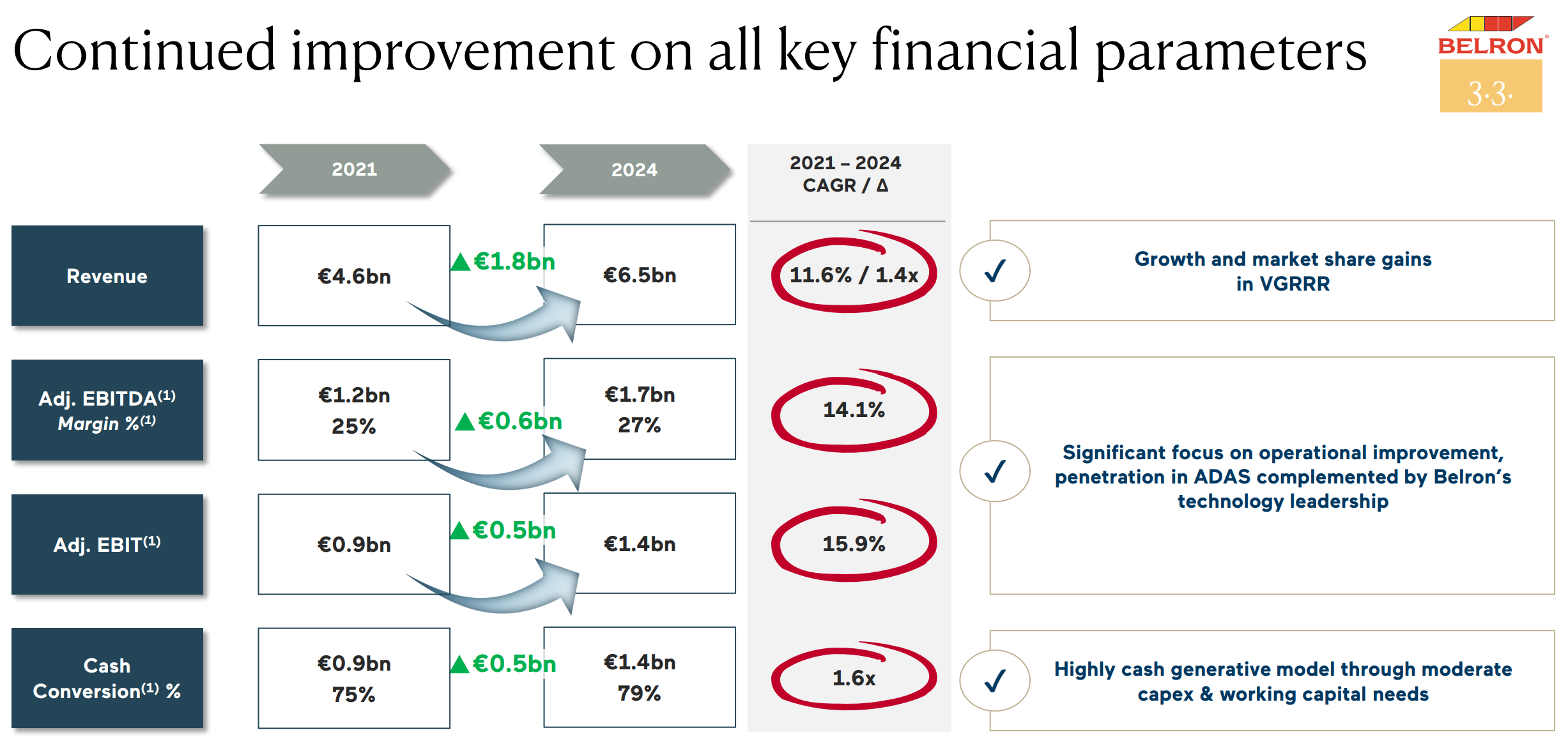

Belron has been a financial juggernaut for the last quarter of a century. Revenue has grown at a c.9% CAGR from 2000 to 2025, with adjusted EBIT margins expanding from 5.4% in 2017 to 23% today with trading cash flow conversion of c.80%. Since CD&R entered the cap table in 2018, growth has accelerated sharply, with EBIT compounding at 16% from 2021-2025.

In 2025, Belron delivered a record year on many metrics: 7.1% top-line growth at constant FX (18 bolt-on acquisitions contributed 1%) and an adjusted EBIT margin of 23%. Looking ahead, management guides to mid-to-high single-digit revenue growth in 2026, with continued margin improvement towards the 2028 target of >25%. The US market is normalising after a sharp period of insurance premium rises (US auto insurance prices rose approximately 40% from 2022 to Q3 2024) drove claims avoidance. Prices are settling (decreasing in places) which should result in more customers making claims through their insurance company again. CEO Francis Deprez mentioned at the FY25 results that the insurance companies are “doing their usual competitive behaviour” again which should be helpful for pricing into 2026 and beyond.

The business is capex-light, cash generative and deleveraging quickly. Net leverage at Belron fell from 5.5x at the peak of the 2024 recapitalisation to 4.5x (€8.4bn net debt) by year-end 2025 (despite paying a €307mn dividend in 2025), with successful loan repricings being achieved on both their dollar and euro tranches. Belron can deleverage at a rate of roughly 0.8x per year. The fact that Belron has operated at upwards of 5x leverage speaks to the stability of the underlying business. I would expect Belron to operate at closer to investment grade level and 3x leverage is probably where it trends to over time assuming Belron IPOs.

Ownership & The IPO

D'Ieteren Group holds 50.3% of Belron, CD&R 20.4%, Hellman & Friedman, GIC and BlackRock hold approximately 18% collectively, and management, employees and the Lubner family (via Atessa) hold the remaining 11%.

Given more than eight years have passed since CD&R first bought into Belron, the case for an exit is clear. The vehicle through which CD&R hold their remaining Belron stake is structured as a continuation fund, which will become five years old in the near term, adding further pressure to crystallise returns, given their lock-up on Belron expired in 2024. The full shareholding list of Belron is as follows:

In the last six months, the IPO chatter has moved from market gossip to credible public reporting. In January, the FT reported that Belron was in early talks for a €24bn IPO (equity value), implying an enterprise value of approximately €32bn, which could take place in New York or Amsterdam by end-2026. In early March, Bloomberg reported that Rothschild had been appointed by D’Ieteren to explore strategic options for its controlling stake, with the valuation range described as upwards of $30bn and close to $40bn. In April, the FT reported that Amsterdam had been chosen as the listing venue, though it noted that no final decision had been made and the deal could stretch into next year. CEO Francis Deprez was careful not to confirm anything, saying recently “we are very happy to be the majority shareholder of Belron. But other Belron investors may want to leave at some point. We will tackle that liquidity event if it happens.”

I think Belron would command an equity value of approximately €30bn in the public markets, consistent with what the financial press has reported. The transaction would likely be primarily secondary equity, though Belron may raise some primary capital to deleverage towards the 3x investment grade target (should be c3.8x by YE26). Amsterdam or New York are the realistic options as the listing venue, with Amsterdam the current favourite although I would have thought New York might make sense given over half the revenue is derived from the US and it might make more sense to report in USD. (Weakening USD was a headwind to Belron reported EUR results in 2025)

Should the IPO proceed, I do not expect D’Ieteren to be a significant seller. Based on management tone, I expect them to retain the vast majority of their stake, potentially taking a modest slug off the table to demonstrate the equity value is real and then most likely return it to shareholders or potentially redeploy while preserving optionality on the rest of the stake.

Other Segments

The remaining businesses are mixed performers. With the exception of Moleskine, all are involved in automotive or industrial parts distribution.

D’Ieteren Automotive: The group’s legacy business and the official distributor of Volkswagen Group brands in Belgium. The business holds approximately 23% market share in Belgian passenger cars. 2023 and 2024 were strong years as post-COVID supply chain disruptions resolved and inventory normalised. 2025 was tougher, with industry sales falling 7.5% and D’Ieteren’s own sales falling 9%. EBIT came in at €232mn, a 14% reduction on 2024 (4.7% margin). The business generated close to €150mn of free cash flow in 2025 and paid an exceptional dividend of €400mn to the parent, ending the year at below 1x net leverage. 2026 should see operating margin temporarily fall below the 4% mid-term target in a tougher market and with less support from VW Group. This is a cash cow at a tough part of the cycle.

PHE (Parts Holding Europe): 91% owned by D’Ieteren. PHE is a leading omni-channel distributor in the independent aftermarket for vehicle spare parts. D’Ieteren acquired PHE from Bain Capital in August 2022 at an EV of €1.7bn (c.7x EBITDA), with an effective equity cost of €571mn. PHE’s 2025 revenue grew 6% to approximately €2.9bn with adjusted EBIT of €267mn (9.1% margin). The business is performing well and consolidating a fragmented European market.

TVH: 40% owned by D’Ieteren (60% by the Thermote family). TVH is the world’s largest independent distributor of aftermarket parts for material handling, construction, agricultural and industrial equipment. D’Ieteren acquired its 40% stake in October 2021 for €1.17bn. Progress since has been disappointing. TVH proved more cyclical than anticipated, was hit by a cyber-attack in 2023, and is currently searching for a new CEO in a tough market for materials handling. 2025 revenue was approximately €1.7bn with adjusted EBIT down 15% to €223mn (13.4% margin). This acquisition has not worked out to date.

Moleskine: 100% owned. Moleskine is an Italian lifestyle brand best known for its notebooks. With 2025 revenue of €117mn, it is D’Ieteren’s smallest business. The acquisition of Moleskine has been a failure. D’Ieteren paid over €500mn for it and the business is currently loss-making, with a pre-tax loss of €8mn in 2025. Ennismore Fund Management, one of the more thoughtful long-term holders of D’Ieteren, characterised the acquisition as spending “over 20% of its market cap on an expensive acquisition of a subscale aspirational consumer brand with no connection to its core or its domain of expertise.“ It is a €600mn lesson the current management team better have learned from.

Central Costs & D’Ieteren Immo: D’Ieteren Immo manages the group’s Belgian real estate portfolio, most of which is occupied by D’Ieteren Automotive, and has a market value of c.€430mn and net rental income of close to €30mn. Group central costs of c.€30mn per annum cover HQ, salaries and reporting. D’Ieteren deserves criticism for poor transparency here by not splitting out their standalone central costs. Overall, these two more or less offset each other from a cash-flow perspective which is likely the reason management bundled them together.

Capital Allocation

D’Ieteren’s capital allocation track record outside of Belron has been underwhelming. Moleskine has been an absolute disaster and TVH has been disappointing. Only PHE, of the acquisitions made in the last decade comes out with any credit as it has executed well against its opportunity. Even Belron, which has worked out, only became an exceptional performer from 2017 which coincided with the ADAS tailwind and CD&R coming on board in 2018 (D’Ieteren sold 40% at an EV of only €3bn!) which leads me to question somewhat the quality of capital allocation at D’Ieteren, especially as they may soon have €15bn of liquid Belron stock to allocate.

D’Ieteren can write equity tickets for new platforms from €200mn to greater than €1bn, targeting business services or light industrials in Europe with scalable models, structural tailwinds and consolidation opportunities. The subsidiaries manage their own bolt-ons within their leverage constraints. My view is that at those cheque sizes, there are simply not enough high-quality opportunities to absorb anything close to the full value of a Belron monetisation. The math strongly suggests a sizeable portion of any Belron proceeds will need to come back to shareholders, including the controlling family, most likely via a special dividend. D’Ieteren has a history of this, paying an exceptional €74 per share dividend to all shareholders in December 2024.

Nicolas D’Ieteren holds 50.1% of the group through his family office Nayarit. His net worth is substantially tied to D’Ieteren’s share price, which is itself almost entirely driven by Belron’s value and he has every financial incentive to see Belron’s value realised fully and returned efficiently. The downsides of a family controlling a Holdco are usually around governance and self-dealing which I am not overly stressed about here. We are investing with Belgium’s second richest family who have demonstrated patient, long-term thinking as exemplified by their quarter century plus holding of Belron, which is to be admired given the many opportunities they likely had to take chips off the table along the way.

I am comfortable enough with likely capital allocation for now. Once Belron is public and D’Ieteren holds a large liquid position, the question of what happens with that capital becomes a key debate for the stock. My base case is that the math forces most of it back to shareholders, the cheque sizes simply do not support full reinvestment and Nicolas's incentives point in the same direction. I am not buying perfect capital allocation here, I am buying a world-class asset at a 50% discount, and the valuation below explains why.

Valuation

My approach is to value D'Ieteren on three components: The NAV of the underlying assets today (via a SOTP valuation with particular focus on Belron), the discount at which the market prices that NAV and how that may develop, which leads to a probability weighted scenario analysis of our likely total return including dividends.

The SOTP value is driven mainly by Belron as it accounts for c.80% of the group’s equity value. Belron doesn’t have any direct comps although there are press rumours that their Swedish competitor, Cary Group could be coming to market soon at a €3bn valuation, which previously transacted in ranges from 20x-25x EBITDA.

So what public comps should we use? D’Ieteren view Belron as a best in class, dominant business services company and would view some of the highest quality compounders in this space as their deserved peers. When looking at a comps sheet, Belron does share a lot of the traits of this grouping, with strong revenue growth (MSD to HSD), operating margins (>23%) and cash conversion which is encouraging. On the other hand, it is debatable whether Belron would garner similar valuations to these groupings from the get-go or whether the market would want to build trust in Belron as a public company first. If we look at high-quality Auto Aftermarket parts companies like AutoZone, O’ Reilly (high teens to low 20s EBITDA multiples) or even leading Business Services companies like Rollins or Cintas (mid to high 20s EBITDA multiples) it would suggest that a high-teens EBITDA multiple, which is what Belron has been transacting for in the private markets, is achievable for Belron in the public markets.

If we look at historical transactions, with credit to Andrew Brown of East72 Holdings for compiling the data, I note that the last two transactions, in 2021 and 2024, both transacted at just under 19x EBITDA.

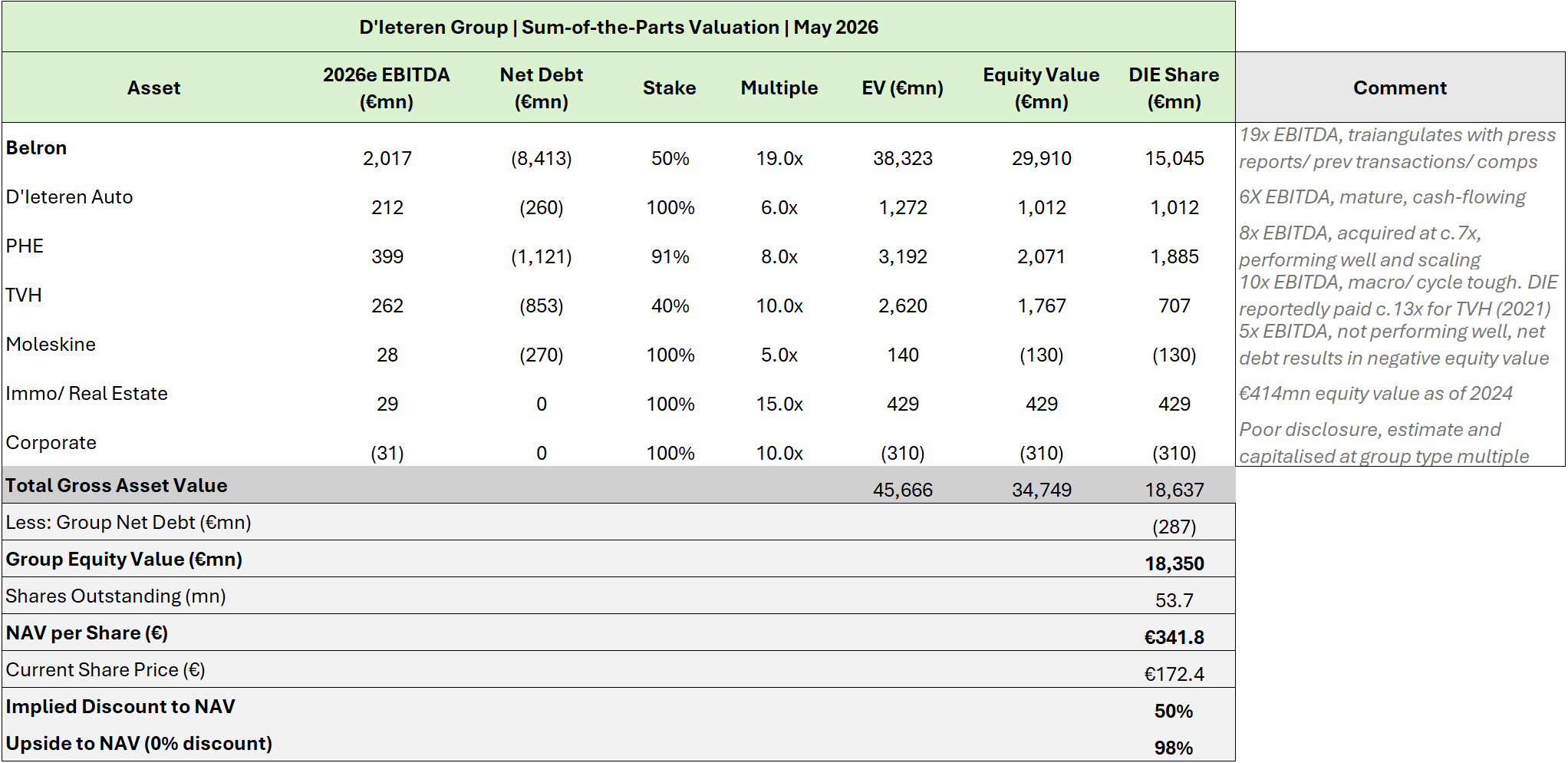

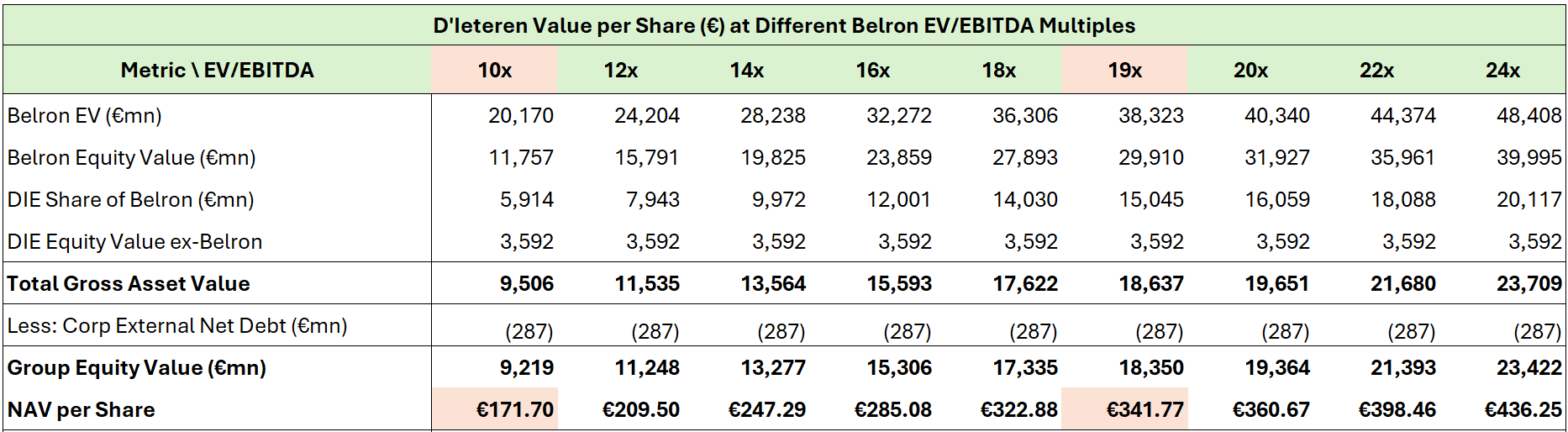

At 19x 2026e EBITDA of €2,017mn I get to an EV of approximately €38bn for Belron and an equity value of approximately €30bn, consistent with the press-reported range, previous transaction multiples and potential comps.

The other assets have been marked at valuations either close to historical transactions, or at reasonable valuations based on the quality of business while taking into account peer valuations. Net debt is accounted for primarily at a subsidiary level with €287mn external net debt at group level as of the end of FY25.

The SOTP results in a NAV for D’Ieteren of just under €342 per share. This compares to a current share price of €172, meaning D’Ieteren trades at just under a 50% discount to my estimate of NAV.

Sum-of-the-Parts

At the current share price, taking everything else at NAV, we are buying Belron at only 10x EBITDA through D’Ieteren. At 19x, D’Ieteren’s 50.3% stake is worth approximately €15bn, or around €280 per D’Ieteren share before any group-level discount. Everything else, after debt, adds a further >€60 per share in net equity value.

Discount to a Discount

Despite a net asset value above €340 per share, most sell-side price targets cluster around the low-to-mid €200s and the stock trades at a discount to those targets again, in the low €170s. A buyer of D'Ieteren today is receiving two levels of discount simultaneously as analysts discount the NAV to get their price target, and the stock then trades at a further discount to that. Why?

The answer is the Holdco discount typically applied to family-controlled companies. A c.50% discount implies either that Belron is worth far less than the market reports suggest, that the cash will never come back to shareholders, or that D’Ieteren’s capital allocation will destroy the value it unlocks. I have addressed all three above. Part of the discount also reflects the fact that Belron is a private company. Investors cannot independently verify what it is worth and so discount the stated NAV accordingly to account for their uncertainty, an uncertainty that a listing would entirely remove. If the discount was partly pricing the opacity then an IPO removes that opacity.

From what I can see, sell-side analysts run a NAV exercise similar to mine, then apply what seems a relatively arbitrary discount that varies from analyst to analyst, resulting in a price target somewhere between the current stock price and their view of true NAV. In fairness, asserting where the discount should settle is a bit of a finger in the air exercise with relatively little proven methodology to guide us. Academic research on Belgian Holdcos specifically identifies four drivers of the discount: the Holdco structure destroys value through costs and poor capital allocation; the NAV is overstated; noise traders push the price below fair value; or the controlling shareholder extracts private benefits of control. I have addressed the first and fourth above. On the second, I do not think 19x for Belron is an overstatement given transaction history and public comps. On the third, noise traders and neglect are real, and a Belron listing would bring a wave of new analyst coverage and institutional attention that addresses exactly that. Forcing price discovery on a major asset is one of the most reliable mechanisms for compressing a Holdco discount.

So where could it settle? Comparable European Holdcos typically trade at discounts of 15% to 40%. The discount reflects real risks around capital allocation, governance, and the reinvestment risk of any proceeds, all of which I have addressed above. While I would not pay a premium to NAV, a discount in excess of 20% applied to a group where 80% of assets may soon be in a listed, liquid stock starts to be excessive. At just under 50%, where it trades today, it feels too wide and I would expect it to narrow over time.

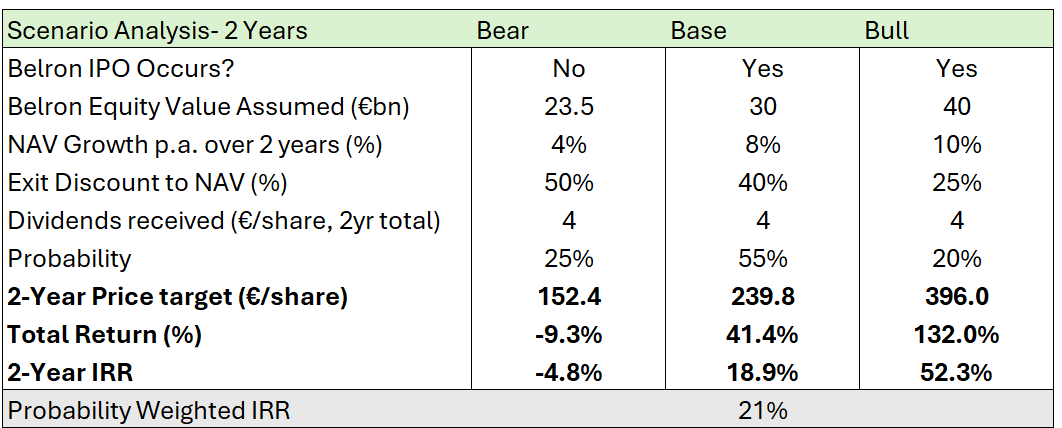

Scenarios

The base case which assumes a Belron equity value of €30bn (19x EBITDA), that NAV compounds at 8% per annum, and that an IPO occurs with the discount narrowing to 40% over two years, generates a c.19% IRR. The bear case, where no IPO occurs and the discount stays at 50%, results in a -10% total return. The bull case, where Belron prices at the top of the range and the discount narrows to 25%, returns 132%. Probability-weighted, the expected IRR is approximately 21%. I like the asymmetry here given I am confident that the downside is relatively limited while the upside has a lot more room to run.

Risks

● No Belron IPO: Market conditions, macro volatility or a breakdown in shareholder alignment could delay or cancel the listing. The April FT report noted that no final decision had been made and that the deal could stretch into next year. If the IPO is delayed indefinitely, the discount is unlikely to compress and the investment case is significantly weakened, though not destroyed, as the underlying Belron value continues to compound.

● Capital allocation post-IPO: If D’Ieteren receives €15bn of liquid value and deploys it poorly, the discount is justified. Moleskine serves as a cautionary tale. The focus on deleveraging, structural constraints on cheque size, and the history of special dividends are defences against large scale capital destruction.

● Governance: Nicolas D’Ieteren controls the group. In 2024, he levered up both Belron and the group itself to buy out his cousin, funded by a special dividend that was taxed favourably for him in a way that was unavailable to most shareholders. While this was a one-time event, there is always potential risk that comes from a single controlling shareholder.

● Macro, trade, tariffs, FX and energy: Meaningful US revenue exposure at Belron and TVH creates vulnerability to adverse trade policy. Energy costs matter given gas is a key input in the glass Belron sources, and a stronger euro is a headwind to reported earnings.

● Cyclicality in the Other Businesses: Both D’Ieteren Auto and TVH are in a cyclical down-turn at the same time, which is putting downward pressure on group PBT.

● Long-term risk from Autonomous Vehicles and EV Risks: A successful roll-out of autonomous cars would reduce accidents and windscreen breaks which would be negative for Belron and more electric cars means less spare part demand for PHE. These are longer-term risks and I would expect the Belron IPO to happen before then!

Catalysts

● Belron IPO announcement: This is the primary catalyst and any formal appointment of underwriting banks or filing of a prospectus would increase focus on D’Ieteren and be a significant re-rating event.

● Capital Return: Even a modest return of capital post-IPO would signal that Belron proceeds will flow back to shareholders over time, likely compressing the discount materially and signalling the latent value at D’Ieteren. A more aggressive buyback or tender offer at current prices would be even more powerful for NAV accretion given the c.50% discount and its announcement would likely compress the discount itself.

● Trading Update and AGM on the 28th May and first half results on the 9th September.

Conclusion

D’Ieteren’s value stems from a world-class, growing asset that is likely to IPO and this value is hiding in plain sight. At a 50% discount to a NAV that will become increasingly liquid, this is just too cheap here. Downside is capped and the upside could be significant once Belron lists and gets properly priced in public markets. I have taken a core position in D’Ieteren and may size it up further into and around the potential Belron IPO.

The above is for informational purposes only and does not constitute investment advice. Always do your own research. If you found this useful, consider subscribing to ValueJunkie for more.